It’s already election season, and we have 15 months to look forward to our politicians each jockeying for position, name calling, debating, all the way to the final two (or three?) we can choose from in November 2016. I am a personal finance blogger, and do my best to stay non-partisan, but when I hear proposals that will affect our tax code or cause me to change my advice on investing, I’m going to analyze it here.

Today, it’s Chris Christie’s proposal to cut social security benefits. First, he’d like to push the age for full retirement benefits from the current 67 to 69. For this part of his proposal, I’d like to address the elephant in the room. The fact that this impacts black men disproportionately from whites.

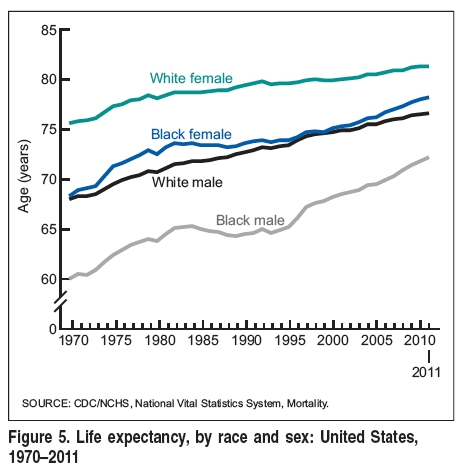

From the CDC, “In 2011, life expectancy at birth was 78.7 years for the total U.S. population, 76.3 years for males, and 81.1 years for females. Life expectancy was highest for Hispanics for both males and females. In each racial/ethnic group, females had higher life expectancies than males. Life expectancy ranged from 71.7 years for non-Hispanic black males to 83.7 years for Hispanic females.”

In other words, on average, a 67 year old black man has 4.7 years left to live, and a white man, 9.3. This cuts the benefit by 42% for black men, but only 21% for whites. I read his proposal and didn’t have to search too long to find government number for life expectancy. Yet, in all the media I consume, all the articles on the Christie proposal, I have yet to see this addressed by anyone. (To my readers – This observation opens a discussion of a far larger issue, health care. In the long term, instead of tinkering with Social Security benefits, we need to close this gap.)

Next, we have his plan to reduce benefits for that he believes simply don’t need the money. How much is that? He would phase out the benefit for those with incomes from $80K to $200K. For a single person, that’s quite the range. In the last election, I recall $250K/yr being considered rich. And we discussed the difference between rich income vs rich wealth. It’s possible to make $250K and blow through every dime, and it’s also possible to make $100K and save your way to a $2M retirement fund. But here, we’re talking about retirement, and the connection between $80K and the wealth it represents is best thought of via the 4% rule. In other words, assuming I spent a lifetime of work saving to my 401(k) and IRA, pretax, it would take $2M of wealth to let me withdraw $80K per year. This takes an above average wage (or wages for a couple, but if one person passes early than the other, we still have a single person dealing with this money) but nowhere near what we consider “rich.”

At $80K taxable, we’ll ignore deductions for this discussion. This person might have as much as $40K in Social Security benefits. The furnace breaks, the roof needs replacing, a child needs help sending your granddaughter to college. Whatever the reason, $60K extra is withdraw from the 401(k). The tax rate this year would be 28%, netting $43,200 to pay a year’s tuition. But Christie would add an effective tax of $20K (i.e. confiscate half the SS benefit) and the net result is $23,200 from that $60,000 withdrawal. This results in a marginal rate of 61.3%.

What I find most troubling is the Catch-22 in which we all seem to find ourselves. Social Security feels like a retirement plan. From the time I started working, I’d get an annual statement, basically telling me that if I kept working to a certain age, 62,65,70, I’d expect a certain benefit. Yet, as many have noticed, the statement have a warning.

Your estimated benefits are based on current law. Congress has made changes to the law in the past and can do so at any time. The law governing benefit amounts may change because, by 2033, the payroll taxes collected will be enough to pay only about 77 percent of scheduled benefits.

This, and the warning that it’s really not a retirement plan, but an insurance, leaves us all encouraged to save all we can, 10-15% of our income being ideal. In my example above, it was more about how the retiree saved than how much. In hindsight, had the savings been post tax, subject to a 25% margin rate, the accumulation might be $1.5M instead of $2M. The tax on dividends would be 15%, as would cap gains. But withdrawals wouldn’t be considered income, and Christie’s horrific proposal could be moot. To be clear, his proposal doesn’t just hit the wealthy, but those who simply saved what they could in a responsible way.

More to come on the topics raised here. What do think about Christie’s proposal? If you agree with him, what am I missing? If not, how would it impact you? Last do you feel that Social Security is a “Entitlement” or do prefer to call it an “Earned Benefit”?

I am not a fan of Christie overall, but the Social Security system does need to be fixed. As a nation we can not go on pretending there isn’t a problem, action needs to be taken on Social Security, but what action?

I think raising the retirement age in inevitable. Americans as a whole, and black males, have longer life expectancies today than 32 years ago when the retirement age was last raised. Raising the age by 1 or 2 years for those under Age 45 today will go a long way. This could be stepped like the 1983 law did as well, having full retirement age change 2 years over the course of 22 years of age. Other ways to fix the gap:

1. Revenue side: tax all earned income for SS.

2. Limit COLAs to chained CPI

3. Slow the benefit growth for the top 50% of earners: Instead of the top bend point going to 15%, have a 10% and 5% bend point as well.

Here is a fun calculator to play around with http://crfb.org/socialsecurityreformer/

Joe,

Good article and raises a number of interesting points. However, I think the numbers you used for life expectancy are not correct. These numbers are life expectancy at birth. The numbers you would want are the life expectancy at age 67. That takes out of the equation those that die young and never make it to age 67. From healthgrove.com, the numbers I found were life expectancy of 20.9 years for Hispanic, 19.1 for non-Hispanic white, and 17.7 for Black (they did not break out by race and sex together). So definitely a spread, but not the dramatic one you showed. I would also be interested to see the life expectancy by class or income, because it would likely show a similar spread, with low incomes having much shorter life expectancy and thus smaller SS payouts.

Thanks, Dave. Excellent point, I missed it completely. Thanks for visiting and commenting.

I agree that SS needs changes, but Christie’s plan is similar to various Democratic plans that fundamentally change SS into an entitlement program. While I tend to lean more Republican that Democrat, I think Christie’s idea is one of the worst given the examples pointed out by Joe.