When I worked for a large company, my wife and I enjoyed the use of a Flexible Spending Account, otherwise known as an FSA. This account allowed us to save up to $5000 pretax, and use it for medical expenses during the course of the year. Doctor copays, medicine copays, and expenses that our insurance didn’t cover, such as chiropractic care. For the most part, I had no complaints about this program. The FSA was a use-it-or-lose-it plan, so members needed to plan carefully, and as the year drew to a close, if there was going to be much money left, it was time to go eyeglass shopping. That purchase was always good for a few hundred dollars. Recent changes to the plan reduced the family maximum to $2500, and tempered the use-it-or-lose-it provision to permit $500 to carry into the next year. Better, but not great.

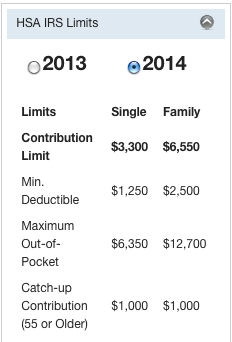

Now, the Mrs is retired and I’m working for a small company whose health insurance is an HDHP, a high deductible health plan. This means that we have at least a deductible of $1250 per person ($2500 for the three of us) and a family maximum out of pocket of $12,700. What this also means is that I was eligible to open an HSA, a health savings account. The HSA offers a maximum pretax deposit of $6,550 per year. Most important, there’s no risk of losing what you don’t spend. In fact, the account offers investment options so if you are young you can use this as a long term savings account, invest it in stocks (whatever funds your custodian offers) and have these funds available for expenses in the future. In a sense it offers the best of both the traditional IRA with money going in pre-tax, and the Roth IRA, as qualified spending allows you to make withdrawals tax free. Unlike the FSA, this account does not need to be sponsored by your employer. So long as your health insurance meets the above criteria, you can open the HSA at a bank that offers it. If your insurance qualifies you for an HSA, check it out. Many of my coworkers were unaware they could use an HSA, and I saved them over $1500 for just a quick conversation and a bit of paperwork.

Right on Joe! I love the HSA. As far as prioritization goes in our investment strategy funding our HSA comes second only to getting the employer match from my wife’s 401K. Who do you use for your HSA? The only place we could find with good investing options was HSAAdministrators.info . The only thing I don’t like about them is that there is a $45 yearly account maintenance fee. I hope to get to the point soon where every bit of money we put into the HSA stays for investments and we pay for routine medical costs and minor medical emergencies out of cash flow.

I use Citizens Bank. As I wrote in that article, the startup process was awful, but I’ve had no trouble since then. I’d still recommend them, with just the warning about the first week or two of opening the account.

There was a $15 startup fee, and $3.50/mo maintenance, similar to your $45/yr. In return, The tax savings to me is over $1500, so I don’t really object to the fees. On a positive note, they offer investments which include Vanguard 500 Index Fund Signal Class (VIFSX), an S&P Index Fund with a .05% expense ratio. I can start using the investment options once the HSA balance exceeds $2600. At this stage of our lives, we’re not rushing to do that, as our expenses this year will probably go over $4000.