Years ago, I started asking questions that seemed like gambling to help understand how others viewed risk. I would ask, “If I offered you the chance to flip a fair coin, but I’d put up $2 and you’d only have to put up $1, would you play?” And then the follow on questions had to do with how much money and the nature of the bets, e.g. one taker said he’d like to bring $100, but make $10 bets, figuring that was the fastest path to wealth. As long as he won 1/3 of the flips, he’d at least break even.

I spent some more time tinkering with this idea, until I read “The Intelligent Asset Allocator” by William Bernstein who introduced the spin on this which was for me the ‘missing link’. Instead of having a coin flip represent a gain of $2 or loss of $1, he suggests the gain as return of 30% and loss of 10%.

This was the difference between a purely hypothetical question, and something that more accurately reflect the stock market.

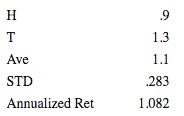

Let’s look at the outcomes for one coin.

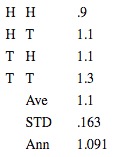

So far, so good, or “so what?” you may say. First, note that while the average of .9 and 1.3 is 1.1, if you have these returns one year after the next, your annual return is (1.3*.9)^.5 = 1.082, only 8.2%/year. But look what happens by “splitting the bet”, half your money on one coin, then half on the next.

What do we gain by flipping two coins? If both show heads, or both tails, the result is still -10% or +30%, but in the two cases where there are both a head and tail, the return is +10%. The chance of loss has gone from 50% to 25%, the Standard Deviation of returns (risk) dropped, and the annualized return has gone up.

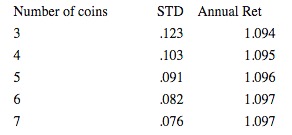

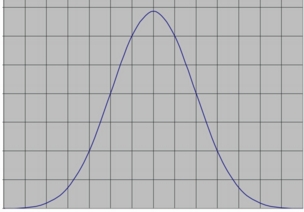

No matter how many coins we flip, the average will not change. We are on our way to constructing data that, when graphed, will form a bell curve. The mean of that curve is a 10% return. The best we can do by increasing the flips per bet is to reduce the standard deviation, which in turn will increase our resulting annualized return. I ran more numbers for more and more coins as follows:

At 8, the calculations become cumbersome as there are 256 possible outcomes. But I believe the point is proven, that diversifying among assets that are not highly correlated is a path toward reducing risk. Along the way, I did continue to add to the data set, following a series known as Pascal’s Triangle. I then graphed those numbers with some pleasant results as shown.