The gold bugs are an interesting breed. They use misleading rhetoric such as “a storehouse of value” and other argumentum ad passiones to convince you to buy. Those who caught any good part of the recent run-up from ’05 to ’12 sure are happy, but only if they sold. Buying gold at the wrong time can leave you with a bad investment for the rest of your life. Gold’s record high was in January 1980, at $875. Inflation alone would put the price at $2400 today. What storehouse of wealth? We are exactly at half that price. If you buy gold in the form of small bars or coins, you pay a dealer premium, and the buy/sell spread can be 5% or more. For those who wish to buy gold, I’ve mentioned GLD, the gold ETF. It started out as trading as .1oz of gold per share, but as with any ETF, there’s an annual expense, .40%, so the 10 GLD shares that represented a full ounce in 2005, now, eight years later, is closer to .97 ounces. The prospectus for GLD states this clearly.

[T]he amount of gold represented by each share will be reduced over time, from an initial 1/10th of one ounce of gold. Because the expenses of the Trust will be offset by the sale of Trust gold, the amount of gold backing each share (Ounces Per Share) will decrease gradually. Each share will initially represent 1/10th of one ounce of gold, but this will decline over time. This reduction in ounces per share will be reflected in the NAV of the Trust.

GLD did not exist in 1980, but if it did, the ounce you held would be .88 ounces, and today, not worth the current $1200, but about $1050. The question isn’t how long it will take the 1980 investor to simply break even, but whether it will ever happen at all. In 20 years, his .88 ounces will shrink to .81 ounces, and the $2400 target will inflate to $4335 given an average 3% inflation rate. Not impossible, just not guaranteed. When stocks are involved, time is on your side. Even if the S&P or DOW index is flat for a time, the dividends will increase your holdings, and you will be ahead long term. You bought at the 1987 high, just before the crash? Less than 3 years later, you were ahead. January 2000, the S&P at 1500? The 13 years of dividends put you ahead even as the index had a tough decade.

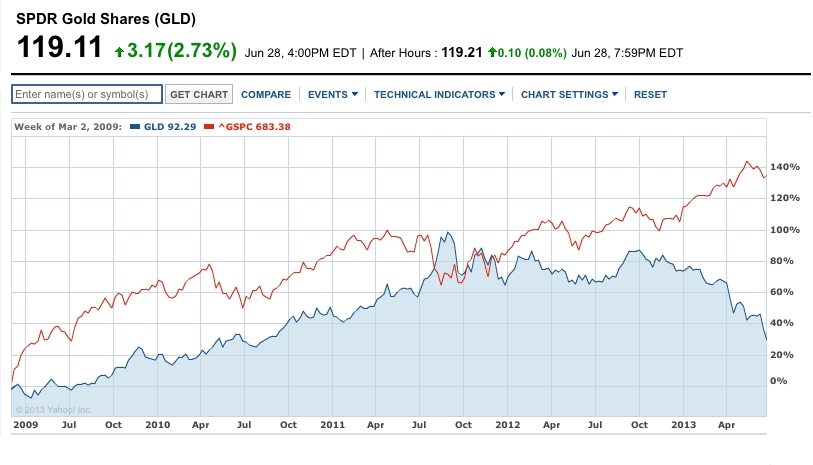

The gold bugs are happy to point out how gold helped their owners get through the stock crash of ’09. And they may have been right, but click to expand this chart to see how they’ve done since. Gold up 30%, the S&P up over 140% (remember to add dividends.)

The gold bugs are happy to point out how gold helped their owners get through the stock crash of ’09. And they may have been right, but click to expand this chart to see how they’ve done since. Gold up 30%, the S&P up over 140% (remember to add dividends.)

The responsible fee-only advisor might suggest that gold is not meant to be used to buy a huge amount and hold for the apocalypse, instead, one should have say 10% in their portfolio, and through the reallocation process, some gets sold in years the S&P outperforms gold, and gets purchased in years the S&P outperforms. I’m working on a study to understand how such a mix would have performed compared to a stock/bond mix or 100% stock investing.

Owning a gold futures contract is not the same thing as owning gold outright, for exactly the reasons stated. Additionally the real benefit of gold in uncertain economic times – the lack of counterparty risk – you also forfeit.

I don’t mention futures here. There is a cost to owning gold. For the small coin buyer, a pretty high bid/ask spread, and cost of storage if needed. The ETF has the commission, which is minimal, but then a .4% expense.

Great post. Like any other alternative investment gold can be appropriate for a small portion of an investor’s portfolio but that’s it in my opinion.

So true. Gold bugs can see gold as the best investment no matter what the rest of the economy is doing. You never hear them say, “It’s time to cash in your gold.” They often use fear of the unknown as a way to convince people to buy it. And they can twist the recent downturn in gold prices to make the case that gold has “hit bottom.”

I agree with Roger, above, that a small amount could be good, but it’s prudent to make it just a small portion of your total investments. Just my 2 cents!