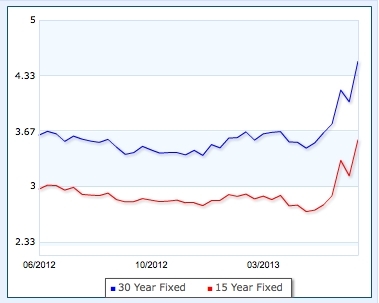

You knew that, of course. If you’ve searched for personal loans at sites such as http://www.cbonline.co.uk/personal/loans you’ll discover competitive rates, but if you own a home in the US and have a mortgage, hopefully you’ve looked at the rates as they dropped and acted by refinancing to a lower rate. But, as I expected, the low rates were not going to last forever and we’ve recently seen the move back up.

This chart only goes back a year. If we went back 5 years, we’d see rates at 6%. Go back to the 80’s and the 30 year fixed rate was 18%. But I digress. The 30 year rate recently hugged 3.4% for a time, and has now risen nearly a full percent from that low.

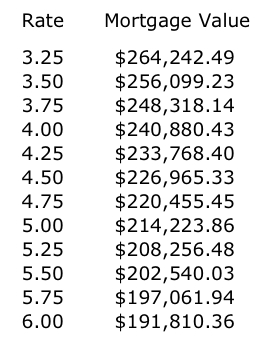

Have I mentioned my love of spreadsheets? You know how there are rules of thumb that suggest you can afford X times you income on your house purchase? Those rules are tied to the interest rate, because as rates change, the payment you can afford gets lower as rates rise. I wanted to look at this with numbers that are reasonable to my readers, so I started with a $60K per year income. This is a bit over median income, and offered just as an example. A well qualified mortgage will permit you to use 28% of your monthly income for the mortgage, property tax and insurance, so I use 23% for the mortgage payment only, that’s $1150 per month. Strictly from an affordability perspective, you can see that at 3.5%, an earner just over median family income would be able to pay for a $256K mortgage. Since this is an 80% loan to value, the home price is $320K, twice the median home price. It was actually a great time to be a buyer. Now that rates are nearly a percent higher, we are close to 4.5%, with that same payment of $1150 only supporting a mortgage of $227, nearly $30K less just a few months ago. This chart gives you a good look at how the borrow power of that payment drops as rates rise. The real question is whether this will put downward pressure on home prices as well. I suspect housing wont drop to meet the new value supported by the payment, but there is a risk that home prices drop a bit from their current levels. This also prompts the question whether rates in the UK will rise and is now the time to check out the rates at http://www.cbonline.co.uk/personal/loans/personal/loans before they head up.

Have I mentioned my love of spreadsheets? You know how there are rules of thumb that suggest you can afford X times you income on your house purchase? Those rules are tied to the interest rate, because as rates change, the payment you can afford gets lower as rates rise. I wanted to look at this with numbers that are reasonable to my readers, so I started with a $60K per year income. This is a bit over median income, and offered just as an example. A well qualified mortgage will permit you to use 28% of your monthly income for the mortgage, property tax and insurance, so I use 23% for the mortgage payment only, that’s $1150 per month. Strictly from an affordability perspective, you can see that at 3.5%, an earner just over median family income would be able to pay for a $256K mortgage. Since this is an 80% loan to value, the home price is $320K, twice the median home price. It was actually a great time to be a buyer. Now that rates are nearly a percent higher, we are close to 4.5%, with that same payment of $1150 only supporting a mortgage of $227, nearly $30K less just a few months ago. This chart gives you a good look at how the borrow power of that payment drops as rates rise. The real question is whether this will put downward pressure on home prices as well. I suspect housing wont drop to meet the new value supported by the payment, but there is a risk that home prices drop a bit from their current levels. This also prompts the question whether rates in the UK will rise and is now the time to check out the rates at http://www.cbonline.co.uk/personal/loans/personal/loans before they head up.