by Joe

on November 28, 2016

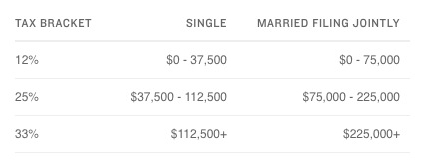

Our new president hasn’t been sworn in yet, but he does have a tax overhaul proposal that has a decent chance of passing. Every change has winners and losers. Even changes that seem positive when first announced. One key provision of the new plan is to bump the standard deduction, from $6,350 single / $12,700 joint to $15K/$30K. Sounds great, right? But as they say, there’s no free lunch, and the personal exemptions are taken away. $4050/yr per person in 2017. Sounds simple, but it impacts taxpayers very differently, based on their circumstances.

- A couple who doesn’t itemize – Their exemption + deduction (E&D) rises from $20,800 to $30,000. $9,200 less taxable income.

- A couple that has $35000 in itemized deductions – They still itemize, but lose their exemptions. $8,100 higher taxable income.

- A 3-child couple who doesn’t itemize - Their E&D drops from $32,950 to $30,000. $2,950 higher taxable income.

- A 3-child couple that has $35000 in itemized deductions. They still itemize, but lose their exemptions. $20,250 higher taxable income.

- Single Parent with 3 kids, taking Std deduction - Their E&D drops from $25,500 to $15,000. $10,500 higher taxable income. Ouch.

The plan also collapses the marginal rate structure a bit.  Â A couple with a taxable $75,000 in 2017 would have a tax bill of $9000 vs the current (2017) $10,317. For the first couple above, the non-itemizer, it’s just gravy, a bit of extra savings. For the itemizers with kids, it only offsets a tiny bit of the high total tax due.

A couple with a taxable $75,000 in 2017 would have a tax bill of $9000 vs the current (2017) $10,317. For the first couple above, the non-itemizer, it’s just gravy, a bit of extra savings. For the itemizers with kids, it only offsets a tiny bit of the high total tax due.

For my family, our deductions are above the new standard deduction amount, so we will see a loss of the $12,150 in exemptions if the new code takes effect. On the flip side, there’s an interesting strategy that might help those who are in a similar position, with itemized deductions that are over this new (proposed) limit. A topic for the next article.

{ }

by Joe

on November 14, 2016

Eight years ago, when Barack Obama was elected president, I heard a clip on the radio. a caller to the Rush Limbaugh show asking for his reaction. “I hope he fails,” were his words. Those words stung me, and stuck with me. Is it possible for a president to succeed and yet, the country be worse off? More important, can a president fail, and the country still be better off? In the end, I was left agreeing with senator Al Franken and forced myself to dismiss this as the rant of one person.

Eight years ago, when Barack Obama was elected president, I heard a clip on the radio. a caller to the Rush Limbaugh show asking for his reaction. “I hope he fails,” were his words. Those words stung me, and stuck with me. Is it possible for a president to succeed and yet, the country be worse off? More important, can a president fail, and the country still be better off? In the end, I was left agreeing with senator Al Franken and forced myself to dismiss this as the rant of one person.

Now, the 2016 election is behind us. My history of comments and Tweets would show that my preferred candidate didn’t win. But as I reflect back to that 8 year old quote, I want to move on, and I want to hope for healing. I want to hope that somehow we are better off in 4 years. That there are more jobs, better jobs, for those that want them. That people of every demographic are able to say that no matter how they felt about who won the election, progress was made, the US is a safer place, that people are respected, and that we worry about the future just a bit less that we did before.

I know that readers expect posts about finance, the economy, taxes, etc. Trying to avoid politics is harder than it should be. Our finances are inextricably linked to what those in our government are doing. I hope, for all our sake, they act wisely.

{ }

by Joe

on November 7, 2016

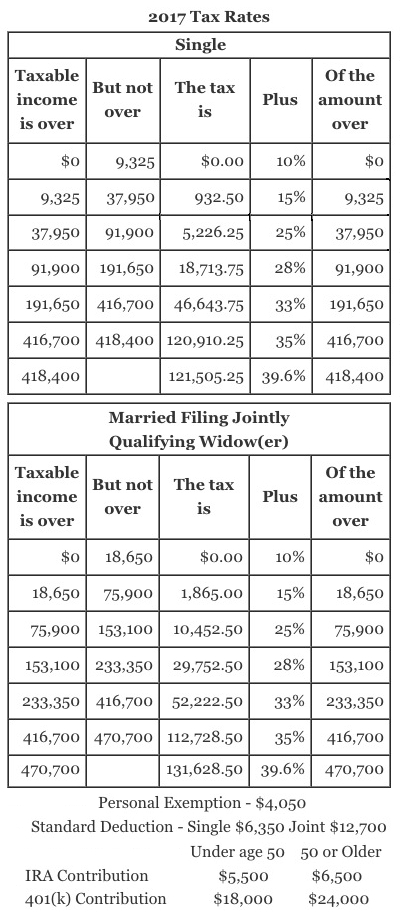

Wow, it’s that time again. The 2017 tax rates have just been announced by the IRS.

The tables aren’t the actual tax you pay on gross income, but on taxable income which is gross less a number of items, including the personal exemption which remains at $4,050 in ’17 and the standard deduction which rises to single $6,350 or joint $12,700, with an additional $1,250 for aged or blind.

Also, note that the IRA and 401(k) deposit limits haven’t changed for 2017.

I’ll be referring back to this article over the next year whenever the tax table is part of the conversation. Check out the new rate table and start planning for 2017.

{ }

by Joe

on November 3, 2016

A brief anecdote that I’ve been meaning to share.

I was at the airport getting my ticket at the counter, and I heard the agent at the next line asking a traveler when his passport expires. He had no idea what she was asking, and said so. “No understand.” The agent repeated the question, once, twice, and then shouting, “What is the expiration date of your passport?!” The man had obvious signs of being in the high tech field, logos I recognized, which had me thinking he was an engineer. But he was Asian, and obviously wasn’t understanding this word no matter how loud the agent shouted.

I felt compelled to do something, so I walked over, looked at him and said,”Sorry. When passport no good?” He repeated my words, looked at the passport and immediately found the date the agent couldn’t see. The passport was put down in front of the agent, the man’s finger pointing, and with a grin, he said,”expiration date.” He then turned back to me and held his arms out, I leaned in and hugged this stranger I just helped. I won’t forget this, or the look on the agent’s face. She seemed unhappy this issue was resolved. I think about that situation now and then, and I’m reminded how sometimes a bit of patience and understanding is all it takes.

{ }

by Joe

on October 31, 2016

Years ago, I was on a business trip. The people I was meeting with were coming to town well after dinner, so I was on my own. The hotel had a nice little happy hour, and I was making small talk with a number of people that I learned were there for the same reason, a real estate conference. They worked for the same company, but hadn’t known each other as they were from different parts of the US. The happy hour came to an end, and I was thinking of where I’d be eating when the group said I was welcome to join, they knew me as well as anyone else there.

I was at dinner with 11 Realtors, long before I had my license, but I had always found the industry interesting. We were ordering drinks when I heard someone tell the waitress, “We’d like separate checks.” I knew this would pretty awful for the waitress, and tried to talk the group out of it. The first objection was easy to address, what if someone had an extra drink? I said I only planned to have one, but even if two people decided to get two drinks each, my share would be less than $2 extra. Then, how, exactly, do we split the check? I thought realtors knew a bit of math, at least the easy stuff. With 12 people, I said it would be easy, we each pay 10% of the check, resulting in 120% of the money including a decent tip. As a group, they weren’t having it. Funny thing, in the end the range from low to high was about $2, not as if a dieter ordered a $12 salad, and someone else, a $40 steak.

When you go out with friends, how do you split the bill? Separate checks, 50/50, or do you do the math to nearest penny?

{ }