The news is out that President Obama is looking to introduce legislation to limit the value of retirement accounts to $3 million. So far, the claim is this targets IRAs, but it’s a simple matter for many of the big account holders to simply transfer from IRA to 401(k), so it would seem logical that once we see the full details, this limit will apply to all retirement accounts.

The news articles are suggesting this limit was a response to the fact that Mitt Romney amassed an incredible $100 million in his IRA. I spent a bit of time before the election writing about Romney and specifically in an article titled Romney’s Enormous IRA Balance – The Smoking Gun I spelled out the issues of how it’s unlikely the account grew to this value naturally.

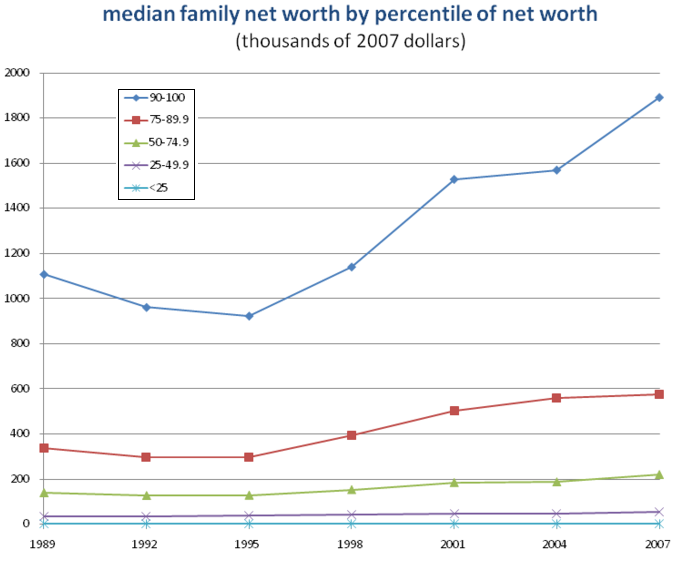

I’m all in favor of Romney’s IRA getting taken apart, i.e. taxed. A current limit of $3 million will not affect the average Joe, take a look at these numbers. You can click the image to enlarge it).

The data is a bit old, but 2007 ended with the S&P just a bit lower than it is now, so for this discussion the chart is fine. We’re looking at median family net worth. For those in the top 10%, half have below $1.9 million, half higher. 5% of families have a net worth over $1.9 million. It’s not too great a stretch to assume that to specify $3M in one’s IRA or 401(k) is some smaller fraction, likely the 1%ers or even a bit fewer. So why all the fuss?

Very simple, remember the AMT. Specifically, I mean you should remember the origin of the AMT. It was created as part of the Tax Reform Act of 1969 intending to target the 155 high income households that managed to pay zero Federal Tax. By 2008, 4% of filers were subject to AMT with 27% of these households having incomes under $200K. Today, $3M still seems like a large number, but inflation has a way of eating away at the dollar. An inflation calculator showed that in my lifetime (50 years) the dollar has eroded by a factor of 7.5X. In other words, something costing $100 in 1962 would cost $750 today. That $3 million IRA cap will feel like $400,000 50 years from now. I know, we can’t forecast a few years out, 5 decades seems crazy. For me, it’s a ‘horse out of the barn’ event. $3M now, but easily adjusted down at congress’ whim.

It’s indexed for inflation. So, that’s not an issue.

I like the idea of going after folks who have, by various tricks, tax-sheltered immense sums. Instead of eliminating all the tricks, this may be a nice way to just go after it on the back end.

Winning one fight is easier than winning all the little loophole fights.

Ultimately I rather see some sort of flatish, no deduction tax, so we can all just get back to focusing our productivity on doing productive things for the nation, vs playing tax games.

The not-indexed-for-inflation timebomb I worry about are the Obamacare taxes.

Obamacare taxes, as currently in effect for 2013, I have no issue with — they’re basically just un-doing the previous huge cap gains and other tax cuts which were overly generous.

But, due to their non-indexing, those could easily creep down into real people’s lives (just like the AMT did).

If Obamacare works, ie starts reducing the runaway growth in healthcare costs and the gov saves $$$ by less emergency room visits to reimburse, etc, then great, maybe it’s all a wash. But that remains to be seen.

I’m sure the administration purposefully didn’t index those taxes because that allowed the numbers to come out especially good when scored across the longer term, I understand the accounting tricks and politics of it, but it could be another AMT.

Thank you for the comment. If it’s indexed, and if congress doesn’t chip way at the figure, I’m ok with it. Still I’m wary of whom we catch in the web vs whom we wish to catch. The Romney type that I don’t particularly care for, vs the regular Joes who happened to work for companies whose stock went through the roof. The $30K (say) employee of Apple who worked in the mail room or as a janitor may very well have put away 10% a year into his 401(k) and now is a 401(k) millionaire. I cite an example, but I know, it can go either way.

Got it. Agreed!

Joe,

Thanks for this level-headed post about a topic that’s sure to get misconstrued in a hurry. It seems there is still a lot that has yet to be disclosed and I’ll refrain from too much comment until then.

However, Brian I’m with you on this comment: “…so we can all just get back to focusing our productivity on doing productive things for the nation, vs playing tax games.”

Right on.

-Christian L. @ Smart Military Money

Joe, it’s all retirement accounts, not just IRAs.

Here’s one article that implies all retirement accounts. http://www.bloomberg.com/news/2013-04-08/romney-s-ira-obama-target-for-revenue-with-3-million-cap.html

Which makes sense based upon their other statements and other tax law.

“The budget will include a new proposal that prohibits individuals from accumulating over $3 million in IRAs and other tax-preferred retirement accounts.â€

http://spectator.org/archives/2013/04/08/obama-attacks-iras

Much thanks, I was working from two less detailed references.

I wouldn’t worry too much about the $3m cap level.

Obama has learned a bit of negotiating 101, he now proposes lower than where he’s willing to eventually settle.

Example: tax rate increase proposal was 200k, ended up at 400k (for single).

Great post about a particularly contentious topic. I do agree that it is part of negotiations to lowball a potential cap, but am with you on the nuances of adjustment.

Once we allow Uncle Sam to screw the guy with $3+ million, then they’ll want to lower it to $2 million, and so on. Keep them away altogether.

Don’t forget that the distributions are taxed at normal income tax rates so Washington still gets their “fair share”. I believe the IRS rate for a 70 yr old is 25.4, so his $100 million IRA distib. is $3.94 million and will be fully taxed at the new Obama rates.

The only legal strategy he could use depends on the legality of “gay” marriage. He could then divorce Ann, marry his son and use the spousal exemption whenever he dies.

Buck, the proposal caps by limiting deposits if over the $3M level, so the Romney IRA stays put, but my Doctor’s IRA cannot accept deposits if too high.

Agreed, it’s a bad idea all around.

This is cat and mouse game, where the rules are written by mice. Closing the loopholes are only affecting unfortunate few who were late to the paradise – saving money from IRS. There is plenty of others left and many more to be opened.

However why somebody is earning $100 million a year is unable to save for the retirement 70% of her/his income, like the rest of us? Isn’t just envy ?