The daily press briefing was held last week and a new proposed tax plan was part of that briefing. What’s strange is that even less was revealed as compared to the details offered during the campaign. This is part of the one-pager that was handed out, the part that discusses individuals. I’m in favor of simplification, but also concerned about unintended consequences of how specific bits of the tax code affect the individual. The first thing I heard, and the sheet confirms, is that the standard deduction will be doubled. I won’t quibble over the use of ‘double’ when the current standard deduction is $12,600 for a couple, and they said $24,000 in the new plan. What continues to disturb me is what would be dropped. The plan says “home ownership,” which to me is both mortgage interest and property tax, yet, in the Q&A they only said mortgage interest.

The new standard deduction would certainly eliminate the need to itemize for a good number of those who do, but at what cost?

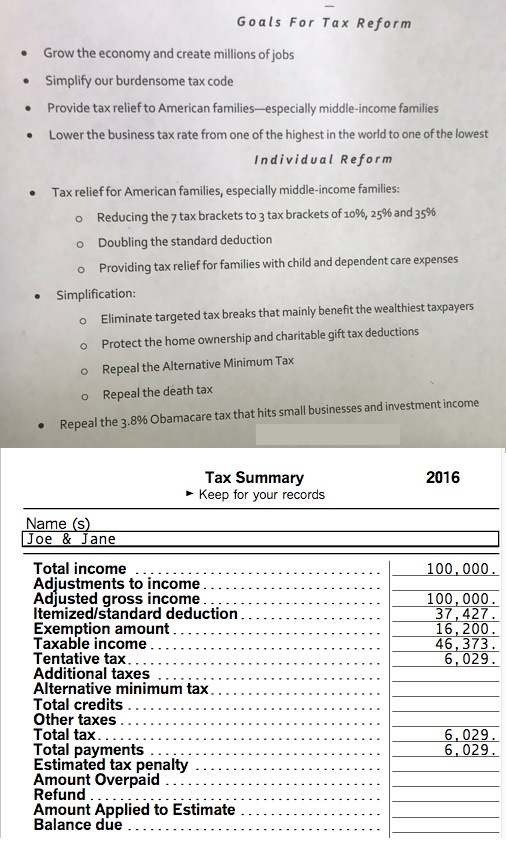

I mocked up a 2016 return for a couple. A professional couple, both with college degrees. Their combined income after their 401(k) deduction is $100K. Their itemized deductions start with the house, $16,000 in mortgage interest, and $8,000 property tax. Their state tax is $3427, and $10,000 in donations. This accounts for their Itemized deductions. They also have $16,200 in exemptions. Net taxable, $46,373, and a tax bill of $6,029.

Now, let’s consider, what we know of the new tax plan. No exemptions, no property tax or state tax deductions. They get to deduct their $16,000 in mortgage interest as well as the $10,000 in donations. This results in a net taxable $74,000, and even though we don’t know more than “3 brackets, 10%, 25%, 35%,” let’s hope for the best and assume the 10% applies up to the $75K first discussed last year. A new tax bill of $7,400.

A few points. This couple had nothing handed to them. In 2015, the average starting salary for college grads was $39,045. If this couple met at school, and their degrees were in STEM (science, technology, engineering, math) they could have started at $110K, combined. Instead our couple is out of school 10 years and has 2 kids. They saved to put 20% down on a $500K house, which is above the country’s average, but not high considering their proximity to the city.

I’ll be the first to say that I understand there may be little sympathy for a $100K couple, but this is just an example.

The $10/hr couple (or $40K/yr) with 2 kids used to have the same $16,200 exemption, plus a $12,600 standard deduction. They paid tax on $11,200 for a tax bill of $1,120. (I know, I ignored child tax credits here, so they may be at $0), but under the new plan, will be taxed on $16,000, for a $500 increase (we don’t know what the child tax credit will be in the new tax code, we only have the one-pager.)

It’s safe to say that repealing the ‘death tax’ won’t help the average American. This tax is likely to affect .2% of estates, that’s just 1 in 500. A couple would need to have assets worth $10.98M on their death before paying a dime in the estate tax. Those who want to eliminate it are the rare top of the economic ladder. Keep in mind, a couple worth, say $10B would pay a tax of nearly $4B. It would take a million families to pay an extra $4,000 to make up these lost taxes. Crazy to just eliminate this.

As we get more details, I’ll offer more analysis of how these changes might affect wage earners at different levels.

20% downpayment on $500K house is impressive. Most people are struggling to get 5-10%.

We are close to $100K couple, so I guess to sympathy. I will be honest with you – there is no extravagance in our budget.

Thanks for the comment. I worked backwards, and calculated that the $400K mortgage would cost $1910/mo which is 23% of the $100K gross. A reasonable amount, even if I’d recommend a mortgage far lower than 4X one’s income. Calling the 20% downpayment was an effort to imply a level of responsibility. The couple are good savers, or were. I heard Mnuchen say that these deductions were skewed to the rich. That may be true, but that doesn’t mean they don’t benefit the middle class as well.

If I could summarize my objection to what I’ve heard of the new tax plan so far, it would be, “The increased standard deduction doesn’t make up for the loss of exemptions, state tax, property tax, and medical expenses.”