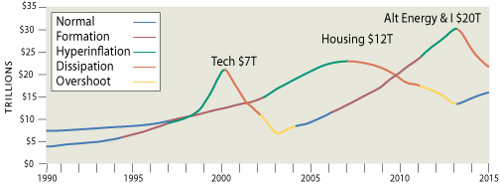

Some time ago, I read a book titled “Pop!: Why Bubbles Are Great For The Economy .” This is not a summary of that book, but I recommend it as it made for some interesting reading. Its premise was that bubbles leave in their wake some new infrastructure (telegraph lines or railroad tracks, as an example) or technology leap (as in the late 90’s ‘dot com’ boom leaving a huge amount of dark fiber and active bandwidth). Now, I put that book down wondering what the next bubble would bring, and perhaps I couldn’t see the forest through the trees. Regular readers know I’m excited about the prospects of alternative energy, specifically, solar energy. Sure enough, Harper’s recently ran an article titled “The next bubble: Priming the markets for tomorrow’s big crash.” In this article, Eric Janszen, the founder and president of iTulip, Inc. speculates that alternative energy may be the next bubble forming, and if his forecast is right, we have years ahead of us to take advantage of the opportunity this presents. This chart offers both historical numbers on Tech and Housing, as well as forecasts for the housing downturn and the Alternative energy bubble.

.” This is not a summary of that book, but I recommend it as it made for some interesting reading. Its premise was that bubbles leave in their wake some new infrastructure (telegraph lines or railroad tracks, as an example) or technology leap (as in the late 90’s ‘dot com’ boom leaving a huge amount of dark fiber and active bandwidth). Now, I put that book down wondering what the next bubble would bring, and perhaps I couldn’t see the forest through the trees. Regular readers know I’m excited about the prospects of alternative energy, specifically, solar energy. Sure enough, Harper’s recently ran an article titled “The next bubble: Priming the markets for tomorrow’s big crash.” In this article, Eric Janszen, the founder and president of iTulip, Inc. speculates that alternative energy may be the next bubble forming, and if his forecast is right, we have years ahead of us to take advantage of the opportunity this presents. This chart offers both historical numbers on Tech and Housing, as well as forecasts for the housing downturn and the Alternative energy bubble.

Joe

{ }

The debate continues about how the subprime mess occurred. Let me tell you how it would not have occurred:

- Maximum Loan to value: 80% any higher requires PMI (Private Mortgage Insurance)

- Debt ratio permitted: 28/36 – This means that one’s mortgage payment and property tax cannot exceed 28% of one’s gross monthly income and all one’s monthly debt burden cannot exceed 36%.

- Income must be verified, i.e. ‘no doc’ loans not allowed.

- ARMs must be qualified at the maximum adjusted payment 3 years hence. This would insure that a year or two of rising rates would not be an economic time bomb.

- All documentation must follow the loan, no matter how it’s sold or repackaged

Would these rules eliminate foreclosures? Hardly. People still lose their jobs, and if unable to find work soon may be unable to make payments. People get sick and are unable to return to work, their disability pay not adequate enough to pay the mortgage. The rules above were broken, and the subprime mess resulted. Follow the rules above and it would take a 20% decline in prices for the lender‘s capital to be at risk. With the permitted debt ratio above, a family earning $60,000 can pay $1400/mo toward mortgage and property tax. A $1200 payment can support a $200,000 loan at 6%, 30yr fixed. 20% down, and this results in a $250,000 home. Now, the median price of a home is $206,200 per the latest CNNMoney report, down from $219,300 in the prior quarter. Seems reasonable to me.

Joe

{ }

Earlier this month, I mentioned the Money Merge Account program on my feature site, and, as frequently happens, I find a magazine article coming to a similar conclusion.

The May issue of Kiplinger’s Personal Finance magazine has a brief article titled “Don’t fall for this mortgage pitch.” It’s a pretty brief article which again questions whether even prepaying at all is a good idea, but concludes with this punchline; “Salespeople challenge whether you’ll follow through on your own – as if spending $3500 for software will ensure that you’ll use it. Tell that to couch potatoes whose high-end exercise equipment gathers dust.” Amen to that.

I’ve also added links to highly trafficked discussions regarding this topic, and also written a stand-alone page comparing one MMA agent’s example to my own approach using a spreadsheet. I don’t know what surprises me more, that the shortcoming of such systems is so obvious, or that people are so desperate they’ll pay $3500 for something they can do with a free spreadsheet. I am happy to send a copy of my MMA spreadsheet to anyone that requests it.

(updated 5/4 – I added the link to the article above as the May issue of Kiplinger is now accessible on the web.)

Joe

{ }

A few weeks back, in the March 7 issue of The Week, I read an article titled “For energy, here comes the sun.” At first glance, it was good to see that I’m not the only one so enthusiastic, nor the only author of bad puns, having titled my first solar story “here comes the sun” back in October. I was happy to discover the article was about futurist Ray Kurzweil’s prediction that he is “confident that we are not that far away from a tipping point (my choice of words as well) where energy from solar will be [economically] competitive with fossil fuels. The longer story appeared on LifeScience.com and was titled, “Solar Power to Rule in 20 Years, Futurists Say“. Kurzweil makes reference to advances in solar power being similar to that of computer technology, but as one of my regular readers Augustine pointed out to me,”Integrated circuits fall in price because Moore said that it would be increasingly possible to shrink transistor sizes, therefore allowing to increase their number per area. And given that the cost of manufacturing integrated circuits relies heavily on the area, the more transistors per area, the cheaper the integrated circuit. Photo-voltaic cells are not made up by Silicon transistors, but by a Silicon film deposited on a surface. Therefore, its area cannot be reduced and its cost is not subject to Moore’s law.” This is true, and resets my expectations a bit. I’m still optimistic that 4 cent/KWH solar isn’t too far away.

Joe

{ }

I recently read someone suggesting this, and it seemed like an interesting idea. Borrowing at a low tax-deductible rate on one’s equity line of credit, to invest in tax free municipal bonds or bond funds, which, after tax, would offer a higher return. One problem, the tax code doesn’t permit this.

From IRS Pub 936, page 4:

Mortgage proceeds invested in tax-exempt securities. You cannot deduct the home mortgage interest on grandfathered debt or home equity debt if you used the proceeds of the mortgage to buy securities or certificates that produce tax-free income.

So, an interesting idea, but not one permitted by the IRS.

Joe

{ }