I’ve been known to use the expression, “Don’t let the tax tail wag the investing dog.” I stand by that remark. If you own a stock and it’s time to sell since it no longer is a stock your own criteria would justify, by all means, sell it. Holding it for an extra month to get long term favored gains may result in a greater loss than the missed long term treatment.

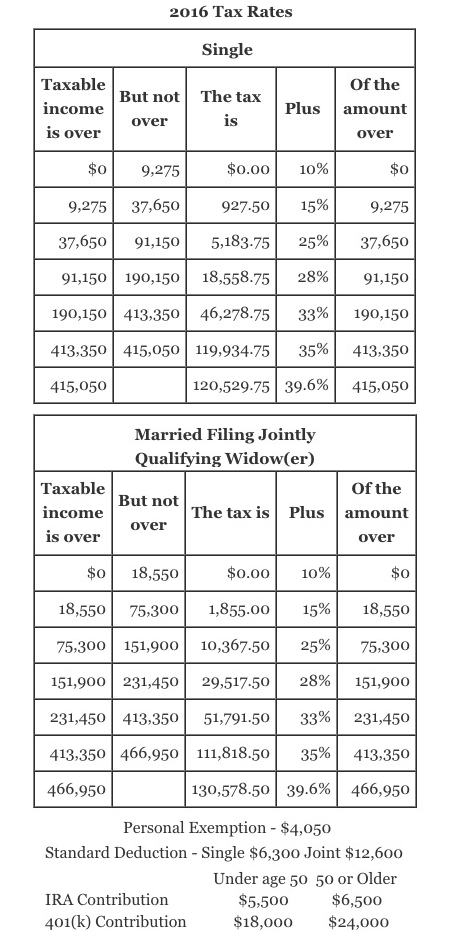

That said, the strategy of tax loss harvesting can help you boost your returns a bit depending on your timing. Let’s look at how this can work for you. First, you need to understand taxation of long term capital gains. There’s a zero percent rate for gains on sales of stocks (including mutual funds) held for over one year. But, there’s a catch. This great rate applies to those in the 10% or 15% brackets. If you take a peek at my last post, you’ll see that, in 2016, for a couple, the 15% bracket ends at $75,300. Add the exemptions and standard deduction, totaling $20,700, and this is an even $96,000, gross income. Less than 25% of households had more than this much income in 2014 according to the latest census data, so this strategy will help most of my readers. Last, understand the rules regarding wash sales. If you sell a stock or fund at a loss and purchase “substantially identical” funds or ETFs with 30 days, this triggers a wash sale. Earlier this year, Michael Kitces wrote an in depth article, Does Tax Loss Harvesting “Almost†Substantially Identical Mutual Funds And ETFs Trigger A Wash Sale Problem? For my purposes, selling an S&P tracking fund or ETF and buying a larger index, whether tracking the top 1000 or 1500 stocks should suffice.

You’re looking at your brokerage statement, and find you have 2 funds, one showing a $3000 gain, the other a $3000 loss. A contrived, simple example. For this discussion, we’ll assume they are generic, say S&P 500 index, and a broad Small Cap fund. If you sold both of these, and bought other funds this year, the loss and gain cancel, no tax due, no tax savings. Instead, sell the losing fund this year, buying into another fund reflecting your desired asset allocation. Now, you have a $3000 (the maximum you can take each year) loss, and you’ll see $450 more in your tax refund when you file. At the end of the following year, review your holdings, and if you won’t have a loser to sell in the next year, sell the one with the gain, and buy into another to keep your allocation to your goals. This move will raise your basis to the new, higher level, and should the market fall from this new level, you’ll have another chance to sell for a loss.

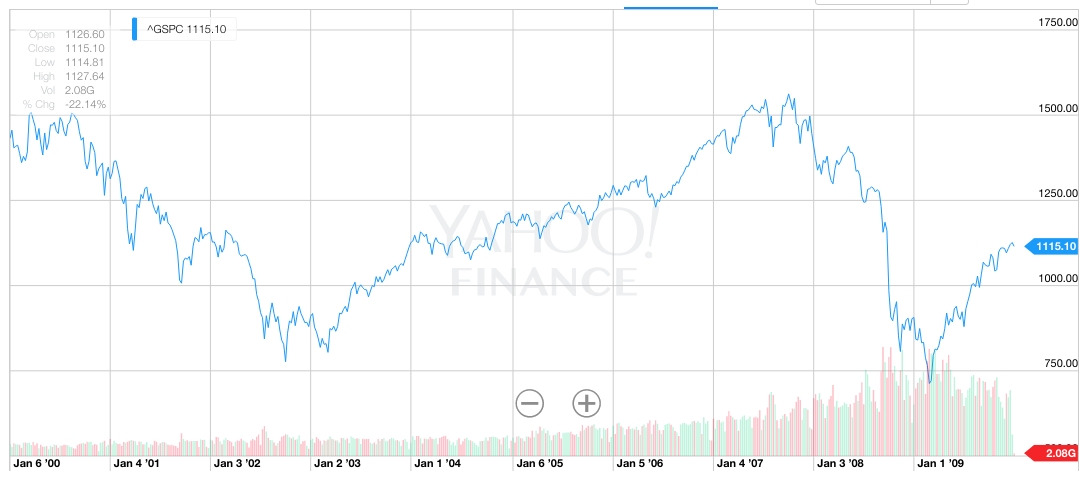

Let’s look at how this strategy could have been implemented over the decade from 2000 to 2009.

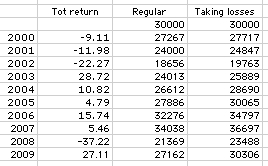

This is the ‘lost decade’ for the S&P, a remarkable 10 years that resulted in the S&P losing 9% of its value. You can click on the chart above to take a look, full size, or go to MoneyChimp and look at the returns for 2000 through 2009. In this crazy decade, we can take advantage of the market’s volatility by taking the losses along the way, and reinvesting this money. This example starts with a $30,000 investment account all reflecting the return of the S&P. For each year from 2000 though 2003 we are able to deduct a $3000 loss and get $450 back when filing. Note, even though 2003 had a gain, the S&P index dropped 40% in the 3 years from 2000 to 2002, and by shifting from one fund to another, there were $12,000 were of losses to claim over the 4 years. In the next few years, basis is increased by swapping funds. Here’s a chart illustrating this –

You can see, the ‘regular’ return reflects the buy and hold, but ‘taking losses’ adds $450 each year we are able to take the $3000 loss. $3000 is the maximum you can take each year again ordinary income. Typically, losses first offset gains, but in our example, we’ll only take losses when they can be deducted against ordinary income. In this decade shown, losses are taken in each year from 2000 to 2003, and again in 2008 and 2009. The gains up to 2007 are used to increase basis by swapping funds, so in 2007, your basis is $36,697. Another fund swap in 2008, results in loss of over $13,000 letting you spread the deduction over the next 4+ years, so even though 2010 and 2011 showed gains, you are still taking a loss and adding $450 into the account.

The result of this annual effort is a 10% swing, instead of losing 9% for the decade, we are up just over 1%. To be fair, with expenses, we’d be just about at break-even, vs being down 9% plus expenses. Another way to look at it is that the return was improved by a full 1%/yr just from this strategy. No magic here, just using the rules of our tax code to write off losses against ordinary income, but take the gains tax free.