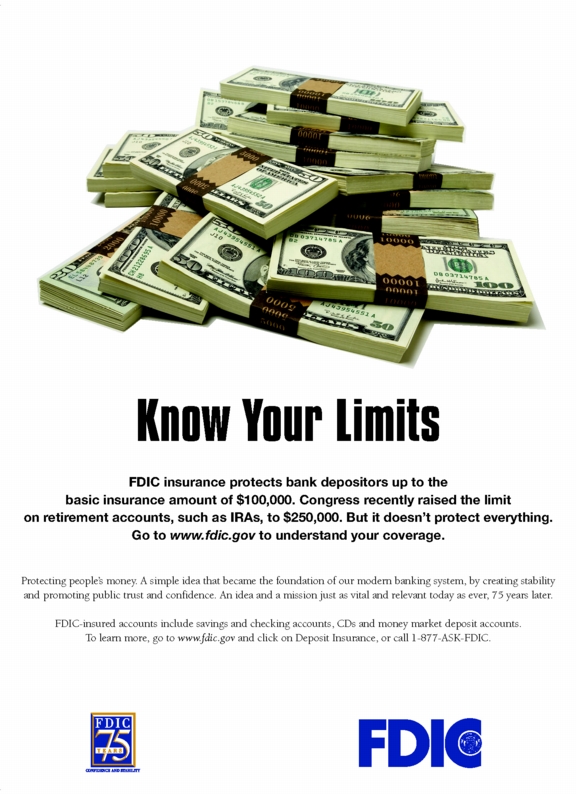

I’ve seen remarks across the blogosphere that the recent FDIC advertisements are a bad sign. I’m not convinced. I think there are many who have no idea how the FDIC protection works, what its limits are, and how to get more coverage. First, here is one of the ads they are running:

The important thing to understand is that non-retirement accounts are insured up to $100K. If you have more cash than this, you should consider splitting it up among more than one bank. In the case of a failure, you may have to wait some time to access your money, so even if you are below the limit, using 2 or 3 banks is a good idea. See the FDIC Website for more details.

Joe

Hi Joe,

As you probably already know, saying that accounts are insured by the FDIC up to $100K is only partially true. Unfortunately it’s a bit more complicated than that.

Certain account types are grouped together at an insured bank (checking, savings, CD’s in one group, then IRA’s in another) and each single account owner is then insured up to $100,000 for the checking/savings/CD types accounts, and up to $250,000 for the IRA type accounts.

Jointly held accounts are split proportionally amongst the account owners to determine coverage limits. For example, a single $200,000 savings account owned by a husband and wife would be fully insured (assuming no other accounts are held at the same bank) because each owner is insured up to $100,000 in that account type.

It’s also interesting to note that an estate IRA (an IRA held in the name of a deceased person payable to a beneficiary) is insured under the decedent’s name and thus isn’t grouped in with the beneficiary’s bank accounts to determine coverage.

A visit to the FDIC’s insurance handy electronic coverage calculator will help you figure out exactly where you stand:

http://www.fdic.gov/edie/

Best regards,

John L.

Again, thanks for writing. I was trying to keep the post itself on the brief side, and provided a link to the FDIC for more details. (This is what I get for not prepping my August main article before month’s end. A couple sub-par blog posts.)

Joe