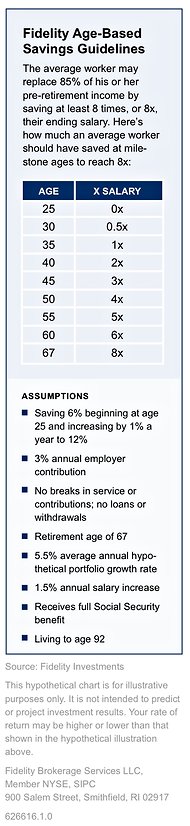

Many articles have been written about the savings you need to have at different ages. In 2009, I wrote my own article Retirement Savings Ratio, which included a spreadsheet to track your own situation. Fidelity recently offered a chart which the New York Times picked up and ran as a story. What’s amazing to me is the numbers are not correct. To be clear, I’m accepting the assumptions Fidelity offers. 5.5% is a pretty conservative growth number, as is a 1.5% annual raise.

Now, when you take the spreadsheet and do a bit of editing, the numbers speak for themselves.

- Zero out savings from 20 through 24.

- Change Annual Raise to 1.015 (this is 1.5%)

- Change percent saved to .15, then manually change the percent to 9 for age 25 and increase 1% each year till age 30

- The above builds in the 3% employer deposit, so all set there.

- Annual return is 1.055 (this is 5.5%)

Sorry if this is a bit tedious, but it’s how you can see the numbers for yourself. The result is that the chart underestimates savings by nearly 50% by retirement at 67. From the spreadsheet I wrote:

| Age | X Salary |

| 25 | 0x |

| 30 | .09x |

| 35 | .75x |

| 40 | Â 2.91x |

| 45 | Â 4.34x |

| 50 | Â 6.07x |

| 55 | Â 8.18x |

| 60 | Â 10.73x |

| 67 | Â 15.25x |

I was tipped off that something was wrong when I saw linear growth, 1x through 6x every five years. That alone told me these numbers weren’t calculated correctly. Growth over time is exponential, not linear. Don’t believe me, pull a copy of the spreadsheet and run the numbers yourself. Most important, don’t believe everything you read. Unfortunately, I can’t get a copy of the underlying spreadsheet Fidelity used to produce their chart, but you can grab a copy of mine.

Keep in mind, rules of thumb are just that, guidelines that apply to people in the center of a range. Some people retire and find that with 40-50 hours more time each week, are spending far more than they did prior to retiring. Others were saving 20% for retirement, 20% went to the mortgage, and 20% or more to college tuition payments. These folk were living on less than half their income. This article was not about calculating your number but about my observation how one pro got it wrong. A future article will discuss your number in greater depth.

Joe, my impression from the Times article is that Fidelity started by calculating the final multiple you would need (8X final salary) to replace final income at 85%. I think they factored in social security and possibly subtracted out the yearly savings from the final income. 8X final income at 4% withdrawal rate gives you 32% of final income from investments. So for instance, a person saving 15% prior to retirement would actually already be living on 85% of income. If spending needs dropped an additional 15% at retirement, they would only need 72% of final income. If social security amounts to 35-40% of final income, plus the 32% from investments gets you to 72%. I think once Fidelity settled on the 8X final income number, they worked backward to age 25 to figure out the track which got you to 8X by age 67.

The other thing that isn’t clear is whether the 5.5% is real return or nominal. They say clearly that the 1.5% raise is over and above inflation. Assuming the 5.5% is nominal makes your spreadsheet much closer to the Fidelity numbers.

Hmmm. I see your point, Dave. My issue is that with the Fidelity assumptions, the 67 year old has a far higher next egg than Fidelity calculates. If their number were higher than my math showed, I’d try to figure if they imply to add Social Security on top.

To be clear, your explanation of why 8X may be a decent target is spot-on. If that was their intent, their suggested assumptions are too high and the worker can save far less to get to that 8X number.

Just saw second comment – The graphic didn’t indicate real vs nominal, but the NYT article did, so I adjusted salary increases to 4.5% vs 1.5%, and market return to 8.5% from the 5.5%.

The result puts the 67 yr old at 14.83X final earnings.

What’s interesting, Dave, is if we adjust earnings, but leave return at 5.5% (or real would be 2.5%) we get a 7.62X final earnings. I know of no planner suggesting a long term return so low. Either way, I am satisfied you helped me narrow down the math Fidelity used, and perhaps I shouldn’t be so critical of a graphic’s lack of full detail.

As always, much thanks for your comments!

Use 3.8% for the annual salary increase. This is per note 8 at http://www.fidelity.com/inside-fidelity/employer-services/age-based-savings-guidelines, as linked at the NY Times site.

Use 5.5% for the annual portfolio increase.

With the 3.8% and 5.5% and a little rounding every five years, my spreadsheet is very close to Fidelity’s.

Got it, Elle. The combined effect of inflating salary above inflation, yet leaving the market return so low actually creates the very strange linear growth that caught my eye. The Times wasn’t as clear as the Fidelity article you linked, as always much thanks.

I think the growth tends linear because the portfolio is normalized by the new salary each year.

Exactly right, Elle. It looked to me like a combination of low growth, or at least lower than the 8% or so I’m used to seeing in projections, along with a decent salary growth.

Agreed that the 5.5 nominal is conservative. Maybe they are assuming 50/50 stocks / bonds with stocks returning 8% and bonds at 3%?

Dave, it could be. I thought the 50/50 returned higher than the average of the two, as the annual rebalance helps to ‘buy low/sell high’ to a degree. Still, I’m grateful you and Elle were able to set me straight. I like the idea of assuming a lower return vs too high a return, but still believe the goal of 8X one’s final salary is too low a target.

Whoever thought growth was linear was forgetting about compounding interest. Sounds like a pretty rookie mistake for someone in the industry!

As Elle and Dave commented, as the income rises faster compared to the return, the curve, while still exponential, is pretty close to a straight line for the years observed.

The numbers I tend toward is to have income rise at or slightly above inflation, but market at 8% or so. It’s this differential that changes the shape of the curve.