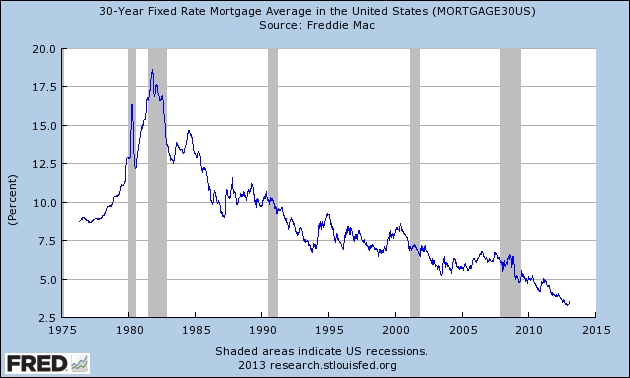

I’ve been hearing more confusion lately regarding how and when it makes sense to refinance your mortgage, and thought we’d discuss it a bit today. First, the obligatory graph –

You can see that as recently as 2009, rates were still above 5% and in the 7’s earlier in the decade. This is well above today’s 30 year rate of 3.4% or 15 year rate of 2.7%. Still, there are people who are under the misconception that a refinance on a 30 year mortgage makes no sense if you are half way through it. Nonsense. (Because on a family friendly site, I’m not supposed to say Bull****) It might be silly to refinance when there’s only a year left to go, but you should do the math and see what makes sense for you.

The way a mortgage is paid off, with a 5% rate, a 30 year mortgage will have about half its balance after 20 years. So, with $100,000 left on that $200,000 mortgage, you find a 15 year rate of 3%, higher than I mention above, but with no closing costs. You see that you were paying $1073 per month, and the new payment will be $690. What to do? Here’s the key point – go back and calculate the payment should you choose to use the new rate but pay it off in the 10 years that remain. You see $965. By refinancing and making payments to stay with the remaining term, you still save nearly $110 per month. Each and every month for 10 years. Not bad for a few hours effort to gather up the paperwork.

Should you take the new payment offered? If you have a car loan or other high interest debt, the extra $380 might help you save quite a bit in interest. Are you depositing enough to your 401(k) to get the full match your company offers? You might deposit that $385, pre-tax and have it doubled on deposit. When 10 years pass, the extra money in the 401(k) will far exceed the remaining mortgage balance. The important factor to consider when comparing loans is how the payments compare when using the same term that remains on the old mortgage. It’s easy to drop your payment by extending the loan to 30 years every time you refinance, but that’s a losing game, at some point you want to put the loan behind you. Tonight I answered a question Are there downsides in refinancing with 5 and 1/2 yrs left? I agreed with the fellow asking the question, it’s a good deal, he’ll save nearly $4000 over the remaining 5 years of his mortgage by refinancing.