by Joe

on February 11, 2008

This month’s Consumer Reports has an article “Your mortgage, It rarely pays to prepay”. They think it doesn’t, suggesting that since the stock market (measured by the S&P) has averaged 10% per year over the last 20 years, that it would make financial sense to choose investing in the stock market over pre-paying your mortgage. On one hand, there’s a neat logic to this. But, as I posted in my blog article Disappointing Results, we see that despite the 11.8% return of the S&P cited by the study, the average equity fund investor only saw a return of 4.3%. In that case, CR might rethink their numbers and their blanket statements offering what may be unsound financial advice.

Whatever you decide, the decision has to be based on your individual situation, your risk tolerance, and investing style.

JOE

{ }

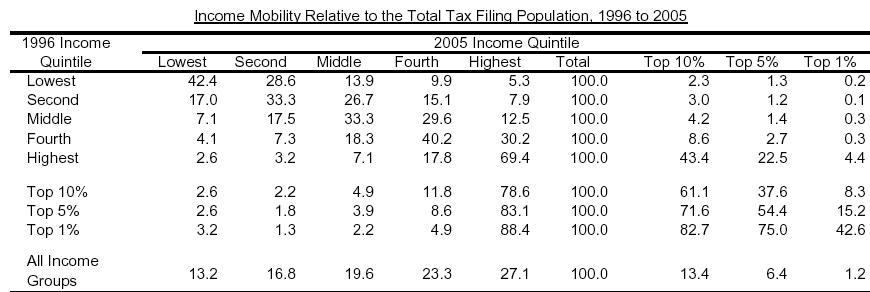

by Joe

on February 7, 2008

A paper titled “INCOME MOBILITY IN THE U.S. FROM 1996 TO 2005” published by the Department of the Treasury this past November was recently discussed in this week’s Barron’s in an article titled “Two Americas, or One“.

One thing that has occurred to me as I’ve read any discussion of income distribution (e.g. the top 1% of earners make X% of income) is whether those people stay at the same levels, the rich getter richer, or whether people move around much. This study helped to answer that question a bit.

Above, is table one from the study. Simply put, of the lowest quintile (1/5) of the wage earners, nearly 58% moved up in income ranking, and 5.3% moved right up to the highest quintile. In a similar fashion, 31% of those in the highest quintile to start, dropped out. You can study this chart to come to your own conclusion, or you may read either of the articles linked above.

JOE

{ }

by Joe

on February 4, 2008

Some time back I made some remarks on my main site regarding some of Suze Orman’s advice. Long enough ago that it now has been moved to The Archives. A regular reader of mine wrote that those posts appeared to be mean spirited, and I edited to change their tone a bit and also stopped with new posts in that direction.

Now, I just had the opportunity to see a CNBC special she did for Martin Luther King Jr. day when my recorder is set to record Kudlow & Co. I must say, she was right on the mark with one great answer after the next.

- Do I pay off the small balance or high interest credit cards first? She replied,”Anyone who tells you to do anything but pay the high interest cards first is an idiot!” Well, right on, Suze. I’ve said this is the one flaw of the ‘debt snowball‘, and I’m glad you agree.

- She advised to deposit enough to one’s 401(k) to capture the company match. Again, I’ve been preaching the same message.

- She advocates Roth for those starting out and how it can serve double duty as an emergency fund, exactly as I remarked last month in my post ‘Roth Magic‘.

- Lastly, she stated most emphatically, that the only people Variable Annuities were good for was the salesmen who sold them.

- I’ll also admit that even though I disagree that one should ever invest 20% of their money in gold, Suze called it right in her advice of July 2006. Gold was about $640 then, $925 now.

I don’t know if she changed her approach a bit or I just happen to catch a good show, but today I liked what I saw.

JOE

{ }

by Joe

on February 1, 2008

I’ve finished up another article for my main site, this month titled BiWeekly Mortgages. I’ll give you the punchline here. I have no objection to paying one’s mortgage down faster if the rest of their investments and debts are in order. Why pay down a 6% or 7% mortgage faster when you owe money on a 15% credit card?

What I do object to is paying a third party or your bank an extra fee plus monthly service charges when you can do this your self. I mention other mortgage acceleration programs such as Money Merge Accounts, which I’m still researching and will discuss here or on the main site in the near future.

JOE

{ }

by Joe

on January 30, 2008

Some time back, I wrote a book review on my main site for Zvi Bodie’s “Worry Free Investing”. I’ve recently been drawn into an online conversation asking about this author’s strategy of investing all of one’s portfolio in TIPS (Treasury-Inflation Protected Securities).

When Professor Bodie wrote his book, TIPS had a real rate of 3% (TIPS have two components – they are tied to the CPI and will rise in value tied to that rate, and also have a ‘real yield’ which is adjusted every 6 months.) and the spreadsheet he offers advises a saving rate of 21% with an eye toward replacing 70% of one’s pre-retirement income using TIPS. Now, as we move to the present, we find TIPS sporting a real yield of 1.2% which, when entered in Bodie’s spreadsheet, now councils us to save at a rate of 34%! As I state in my book review, this hardly seems ‘worry-free’ to me, as someone who was on the plan at 21% now needs to bump his savings by over 50% or miss his target retirement goals by as much.

I also need to mention that the entire return is taxable. If one is in the 25% bracket, 1.05% of that total 4.2% is lost to taxes and leaves a real return of only .15%. To be fair, he does state that these securities be held in tax-favored accounts. I find it curious that in a recent Business Week interview Prof. Bodie maintains his TIPS focus, although he does suggest an S&P call strategy which presumably will juice yields a bit. Such a strategy is not for the feint of heart.

I sent him a question, through his Worry Free Investing Site, I don’t know if he monitors the blog there, or will offer a reply.

As an alternative to this strategy, I’d offer DVY, the iShares Dow Select Dividend ETF which currently yields near 3.7%. That dividend is taxed at favorable rates, 0% if you are in the 10% or 15% bracket and 15% if higher. So 3.15% worst case. I have every reason to believe the stocks in this ETF will keep up with inflation, and for this strategy, that’s all we are asking of it.

JOE

{ }