Congress approval rating is at an all-time low, the IRS is actually far more popular in the last polling. Interesting times.

Congress approval rating is at an all-time low, the IRS is actually far more popular in the last polling. Interesting times.

Given the recent events in Washington, it’s appropriate to start this week with Roger Wohlner’s Some Stock Market Perspective amid the Government Shutdown. Roger talks about the long term, and how short term bits of news or craziness in Washington get lost in the noise when we look at decades of data. Check out his article for the beautiful charts he’s posted, but stay to read his insightful commentary.

A Thank-You to J Money, my McDonald’s Budget article was featured at Budgets Are Sexy this week in J’s Rockstar Roundup: Billionaires, Weirdos & Drug Dealers. (Disclaimer – I am not, nor likely to ever be, a billionaire, nor am I a drug dealer. At times, I’ve been called weird. I plead, no contest.)

At Get Rich Slowly it was time to Ask the Readers: What’s the best way to prepay your mortgage? The reader asked about making bi-weekly payments on her mortgage. I have no objection to setting money aside to make extra payments if that’s what you’d like, but I advise never to pay extra to service the bi-weekly payment. Just send in the extra funds as they accumulate.

Who Really Needs Your Social Security Number? This was the question that was answered at MoneyNing this week. It’s not a number you should give out to anyone that asks, there are really a few select times it’s actually required. Emily explains when to just say “no.”

Just when I thought I’d never reference Soylent Green again, Frugaling.org posted Soylent: The Future Frugal Food Source. It seems a company has appropriated the name Soylent and is manufacturing an inexpensive source of nutritious food under this name. To be fair, the Soylent website offers a discussion of food waste and cost. This product has the potential to reduce the issue of starvation in the world. If you visit the site, you’ll note the founders of the company are young, too young to have seen the movie in the theaters. It’s we who are 50 and over who will be a bit grossed out by the name of this product.

And from Time Management Ninja – Why Being Right Isn’t Always the Most Productive Answer. I offered my own comment, agreeing with Craig that time is important, and sometimes moving on is far more important than being right. The debate can be a productivity killer. I’ve seen it happen time after time.

I admit it. I don’t understand politics and government as well as I wish I did. No secret, the government is shut down. So why is congress still getting a pay check?

If you have a teenager in the house, you’re likely to hear the expression,”that’s the stupidest thing I’ve heard in my life.” A few things come to mind, “I guess you haven’t listened to some of the people I worked with,” is one, but I can’t keep from saying,”make a list and see if the next stupid thing you hear actually tops it, and so on.”

When it comes to the mistakes investors make, I’m sure the list is long. It probably starts with spending more than you make which results in simply not saving at all. Then comes not saving nearly enough because most people don’t actually go through the exercise of calculating their retirement needs. For those actually investing, a major error is the propensity to buy high and sell low. I wrote about this in Disappointing Returns sometime ago and described how for the 20 years ended Dec. 31, 2006, the average stock fund investor earned a paltry 4.3 average annual compounded return compared to 11.8 percent for the Standard & Poor’s 500 index.

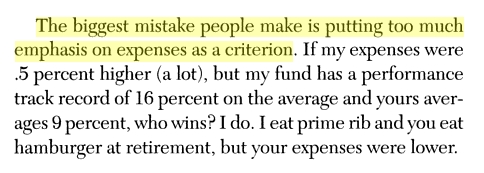

More recently, we discussed Frontline’s The Retirement Gamble, a PBS broadcast that focused on cost, how a 2% fee in one’s 401(k) would wipe out nearly 2/3 of your returns over time. If you use an advisor and find that his (or her) personal advice is worth a fee, that’s a different story. I’m strictly talking about ETF or mutual fund expenses. That said, I present you with the stupidest thing I’ve heard a financial author say. Ever. This may change, of course, but it’s the benchmark against which I’ll hold other foolish quotes I find for the rest of my life.

This is from David Ramsey’s Financial Peace Revisited. And I’m a bit taken aback. There are two implications here. First, that there’s a positive correlation between expenses and returns, as if to say “you get what you pay for.” This was disproved years if not decades ago. The second, and even more dangerous implication is that 16% is a number that one can ever see long term. The 80’s and 90’s (remember those years?) brought us a whopping true compound return of 17.99%/yr. But, of course the next decade’s fiasco brought the 3 decade average down to 11.29%. A look further back brings us closer to an even 10% CAGR. 10%. Not 12%. And certainly not 16%. Consider, at 16%, investments double in 4.5 years. 45 years would result in 10 doubles or your investment growing 1000 fold. Imagine putting $1000 away each year for your 10 year old knowing that starting at 55, she’d be able to withdraw $1,000,000 each year. Sorry, not going to happen. And when it comes to finance, hyperbole has no place in the discussion.

Sorry, Dave, expenses matter, .5% per year over one’s investing lifetime adds up to a sizable fraction of their account. Hopefully, you’ll have the patience to understand this and withdraw these remarks that can damage your followers’ hard earned savings.

A busy week, with some great articles to discuss. At Bargaineering, Miranda gave some guidelines on How to choose between a traditional 401(k) and a Roth 401(k). It takes a bit of math and analysis to calculate the better option, and Miranda’s advice helps provide some insight to this process.

At Monevator, Why I’m not paying off my mortgage. The math is simple, his mortgage is currently 1.24% The Accumulator is comfortable his investments will beat this rate long term, so instead of paying off the mortgage, he’s staying fully invested. This issue has people on either side and a whole bunch in the middle. I’m in the group that will be paid off before retiring, but not in a rush to accelerate payments to end it sooner. How about you?

Len Penzo tells it like it is, he doesn’t mince his words. And it seems neither do guest posters at his blog. This week, Joe Saul-Sehy advises, Don’t Be a Moron: How One Man Paid $87,500 in ‘Moronic’ IRA Fees. You read my delightful and informative article A 401(k) is not an investment? This one could be a great follow up to it, alternately titled “An IRA is not an investment.” Against all the good advice Joe S had to offer, a client “cashed out” his IRA, and was left with a huge tax bill and penalty. The title was slightly misleading, to me a fee is something else, but the story brought a tear to my eye as I considered how many hours the story subject must have worked to earn this money, and it was gone with one stroke of a pen.

At I Heart Budgets, Jacob asked a question – What’s Your Percentage? He’s saving 6% of his income and would like to increase this number to help pull in his projected retirement date. A nice goal, Jacob.

Ninja at Punch Debt in The Face tells us, “I hate paying for things that we don’t use.” I don’t blame him. It’s bad enough to spend money on the necessities, but to see it go towards things you don’t use is just awful. No Netflix for me, either, Ninja.