This week, a failed attempt at a filibuster to undermine funding of Obamacare. It still passed.

This week, a failed attempt at a filibuster to undermine funding of Obamacare. It still passed.

A guest post from Crystal –

We live in an amazing era of unparalleled convenience, thanks to the Internet. With just a computer and a connection, you can correspond with someone on the other side of the globe, or buy groceries and have them delivered right to your doorstep. You can even pay your bills, manage your money, and take care of all your budgeting needs without leaving your desk. In fact, there are so many online outlets for doing so, it’s a bit confusing figuring out where to start.

Of course, the Internet is also a top resource for finding the necessary information to answer such questions. If you’re just beginning to test the waters of online financial applications, we recommend visiting these sites for starters.

Image via Mint.com

Considering the vast assortment of online finance-advice outlets out there, why not start at the top? Most visitors consider Mint.com to be one of the best money-management tools available on the Web. Its greatest strength lies in the broadness of its potential application and the simplicity of its design. The site monitors your transactions to paint an exact picture of your current budget, and presents the results to you with no frills or mess, emphasizing easy readability.

Image via Geezeo.com

Simple, no-frills information is a definite plus. That said, another major strength of the Internet lies in its social aspects, and its ability to foster a community. Geezeo.com is a financial site that draws upon that strength, giving users the power to seek advice and tips from one another. The website also offers investment and budgeting services similar to those of Mint, but it truly shines for its tailored expert advice and community reviews.

Image via HelloWallet.com

It’s tough to beat the professional quality of established sites like Mint and Geezeo, but recent startup HelloWallet is a strong contender, offering a refreshing, independent take on financial planning. Like its peers, the site offers comprehensive budget planning in an easily digestible package for the average layperson. However, using its custom software, it also boasts powerful forecasting potential. Besides tracking your transactions and goals, HelloWallet will adjust on the fly based on recent changes in activity or projected patterns.

Image via AnnuityAssist.com

If you’re asking yourself, “How does a variable annuity work?†This site will help you sort it all out. The topic of annuities is fairly complicated, so it makes sense to seek help with it on the Internet. Unfortunately, though, a lot of annuity sites are thinly veiled sales pitches, or worse, pressure you into giving them your personal info in exchange for any sort of service. What if all you’re looking for is a bit of education? You can find what you’re looking for on AnnuityAssist, for one. The site provides educational annuity assistance for free above all else — it does offer options for paid services, should you want them, but doesn’t force them on you.

Image via Buxfer.com

Not all budgeting tasks are solo activities. In fact, managing money for the sake of a group can stand out as more complex and difficult than most financial tasks, and can involve hurt feelings and stepped-on toes if you’re not careful. Luckily, sites like Buxfer exist to help you out here. The site tracks expenses and IOUs among various members in a group, and is perfect for handling all sorts of potentially sticky situations, from splitting a restaurant bill to covering expenses for an international vacation.

Image via WePay.com

Another good example of a site that emphasizes group budgeting is WePay, which offers many services similar to those of Buxfer. However, it specializes more in budgeting for small businesses, charities, and other organizations. This site is a valuable resource for the tech-savvy small business owner, providing tools to handle customer transactions and keep track of where your money’s coming and going.

Image via SmartyPig.com

Sometimes the smartest thing to do with your money is to simply save it. It’s no longer the norm to keep your cash in a piggy bank, but SmartyPig offers a modern, electronic take on the concept. The site helps you set up a savings fund with a specific end goal in mind, such as a vacation, a wedding, or a big-ticket item. It will then track your progress towards the desired amount, encouraging you to keep building up your nest egg until it’s ready to hatch.

In your quest towards better budgeting and financial sense, perhaps your greatest asset is information, and the Internet has that in spades. Take a look through a few of the above sites, and arm yourself appropriately to give yourself the confidence to manage money like a real pro.

Sources:

http://www.geeksugar.com/Websites-Track-Money-Finances-18794219

http://www.kiplinger.com/article/spending/T007-C000-S001-the-six-best-budgeting-sites.html

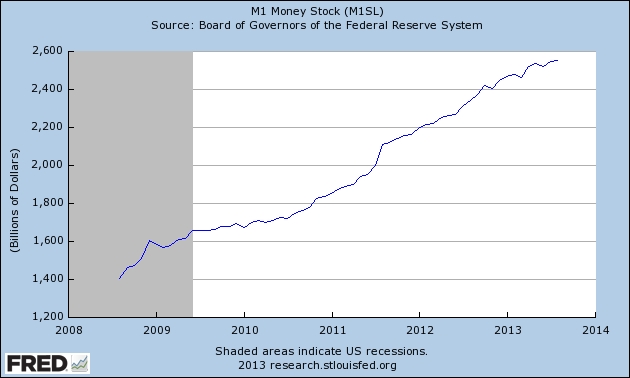

We talked about the Taper, today, I’ll share my bigger concern, the potential wave of inflation. We first need to understand a couple things. First, a look at M1 –

From the end of the recession, M1 (Defined as “M1 includes funds that are readily accessible for spending. M1 consists of: (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) traveler’s checks of nonbank issuers; (3) demand deposits; and (4) other checkable deposits (OCDs), which consist primarily of negotiable order of withdrawal (NOW) accounts at depository institutions and credit union share draft accounts.”) has gone up by a Trillion Dollars, or over 60% in just about 4 years. This doesn’t tell the whole story. We need to look at Velocity –

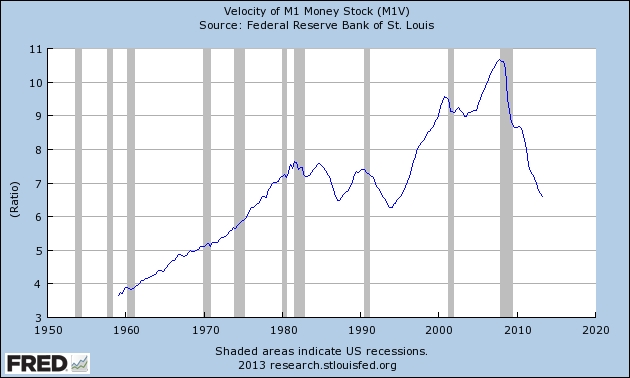

Velocity is the reason why the required money supply doesn’t need to equal an entire year’s GNP. It’s defined as the average frequency with which a unit of money is spent on new goods and services produced domestically in a specific period of time. The time unit is nearly always defined as one year. So, we stare at the growth of M1, but see that velocity has tanked. We exited the recession with about $1.6T in ‘cash’ times about 9 giving us a result of $14,4T. Now, M1 is nearly $2.6T, but velocity has dropped to 6.5 resulting in $16.9T. Barely a 17% increase over 4 years time. (Note, GNP is running at just over $16T for the year, so my eyeballing the numbers here is resulting in a bit of rounding error.)

I don’t know when the economy will gain some steam, but it will happen eventually. When that happens, velocity will go back to more normal levels, and that will potentially create a wave of inflation that will catch many by surprise. But just as the banking crisis was predictable, so is this. The only way to avoid a highly damaging level of inflation is for the Fed to quickly drain excess liquidity. So as we move forward, the money supply is an important part of the equation, but don’t take your eye off velocity. It’s the indicator that will tell you whether the Fed has to act, and act fast.

We are living in interesting times. The Fed Funds Rate is targeted at 0-.25%. The last time it was this low was in the late 1950’s, so it’s fair to say that for most of us, these are the lowest rates we’ve ever seen. As I became interested in finance in the late 80’s, fed funds rose from 6% to 10% before starting its long decline to where we are today. In a grad school economics class I recall a discussion on monetary policy, and the question came up – If the Fed Funds Rate ever went to zero, what tools would the Federal Reserve have to push the economy out of a recession?

We saw the answer. It’s called quantitative easing. Instead of simply driving interest rates down, the Federal Reserve began buying mortgage backed securities, 40 billion per month in the early rounds, now, also long term treasury bonds for a total of $85 billion per month. In effect, this is money being printed and pumped into the system, in the hope that this money will help to spur the economy. The results appear to be a bit questionable. Last August, I wrote Cash Hoarders – QE3 won’t help, in which I discussed the enormous cash hoard that U.S. companies have in their coffers. If their $2 trillion dollar nest egg isn’t encouraging them to expand their businesses and hire more workers, why would QE cause them to behave any differently?

Interest rates on mortgages are also at near record lows, but many who desperately need to refinance to take advantage of these rates are unable to secure a new loan. The banks are requiring higher FICO scores than they did years ago, and people are still stuck with under water mortgages at rates far higher than they should be paying. The money that’s pouring our of the Fed appears to be propping up the stock market, but doing little to help the economy.

Now, for the Taper. When the Fed is satisfied that the economy is on track, as measured by a lower unemployment rate and improving GDP, they will reduce the purchases. Not bring them to a halt, not reverse their position, just Taper a bit. For some reason, the prospect of this happening freaks the market. To be clear, QE which the Fed says is needed because the economy isn’t really as healthy as it should be, and will slow down as the patient improves. But the market prefers the bitter medicine instead of a healthy economy?

Next (on Thursday) – The Velocity of Money. This little understood phenomenon is part of the potential wave of inflation that may occur after QE ends.

This week, The Bernanke, along with the Federal Reserve, decided the economy wasn’t growing enough to end QE, and would hold off on the taper. The market breathed a sigh of relief and rallied on this news. We’ll talk more about QE and the Taper this coming week.