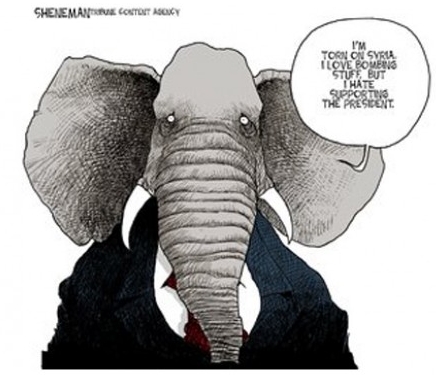

Congress will have a tough choice this week. I hope they choose wisely.

Congress will have a tough choice this week. I hope they choose wisely.

A guest post today –

Investment dollars have been pouring into rental property over the last few years.

Institutional investors have been big buyers of real estate to rent – finding the yields higher than elsewhere in the market and property prices reasonable following the recent housing crisis. The wide interest has been highlighted (or capped?) with Deutsche Bank and Blackstone’s recent offering of bonds backed with rental property assets.

Individual investors have also been keen to grab to rental property as investments, particularly those confused and frustrated by losses in the stock market. Many use a common justification that goes something like: “I want to invest in something I can touchâ€.

Case in point: we at Guide Financial recently met Kumar while doing software testing. He is a well-paid IT consultant, but doesn’t hold any money in a retirement account. Instead, he gathered all his money in 2008 and bought a second house, which he now rents out.

He expects that his rental income will provide all the financial security he needs in retirement. His justification – “I can see and understand a house.â€

But how does a house as a retirement asset stack up in a careful comparison against more traditional options?

The benefits:

Nice cash flows – Like bonds, or high-dividend stocks, rental properties provide steady cash flows, clearly ideal for people approaching retirement. In recent years, the yields have exceeded those available on other assets, widely above 5% in the US through the beginning of 2013.

Inflation protection – The other great feature of rental property is that it is effectively indexed to inflation. As prices rise in the economy, you can usually pass rent increases on to tenants. This combo of high yields and inflation protection is rare in fixed income securities.

Tax benefits – Landlords can deduct many of their big expenses on properties including mortgage interest, house depreciation and many expenses related to the management of the properties. The value of these benefits can be significant.

The downsides:

Big market risks – Property may be tangible and give people the feeling of security, but this doesn’t mean that it provides returns that are more stable or safer (anyone remember 2007?). When you invest in rental property you are assuming large market risks. The factors that affect property values are complex and unpredictable – just because rental prices have been increasing for the last few years this does not mean they will continue to do so. In fact, many analysts think we may be nearing the peak of a “rental bubble.â€

No diversification – Just as home prices don’t offer returns that are any safer than most stocks, a house is going to be a huge part of any average person’s total portfolio. For retirement, most financial planners will suggest that you maintain a diverse set of assets, to lower the likelihood of big losses for similar return potential. If you have a house that is 80%+ of your portfolio – your eggs are effectively in one basket. You’ll be taking a lot of risk you aren’t hedged against, for uncertain returns.

Illiquid – If your retirement stocks are falling in value, it’s easy to sell them. But selling your house is a huge headache, takes a lot of time and is very expensive (often up to 5% of the home’s value). Real estate is not liquid and creates additional risks for someone trying to use it as an investment.

Tax advantages complicated and not the biggest – While significant, the tax advantages from rental property investments are typically going to be less than those offered by retirement accounts like 401ks and IRAs. They also require a lot of complex accounting that will create substantial extra work for you. If you are saving for retirement, you’re probably better off minimizing taxes through investing in a 401k or IRA than putting money in rental property.

Managing property is a headache – You probably don’t want a full-time job in retirement, but managing a property can come close to taking a similar amount of time. You’ll have to deal with deadbeat tenants, frustrating repairs and time-consuming renter search processes.

The verdict:

A few years ago, the economic environment may have offered conditions that made rental property an attractive choice for investment. Now, rental yields are coming down while housing prices and mortgage rates rise. If you don’t have a large portfolio that makes owning a home a potential small piece in a broad mix of other assets, then it may be good to sit out the rental income property craze and focus on building other more traditional assets for retirement.

Interested in learning more? Look for more personal finance insights at

Blog.guidefinancial.com and follow us on Twitter @guidefinancial

Scott Burns, CFA covers personal finance for issues for Guide Financial, a San Francisco-based startup offering unbiased, comprehensive and affordable financial guidance to the millions of Americans who don’t have access to high-quality advice.

It seemed interesting timing that I caught this political cartoon soon after my article on the McDonald’s budget was written. For what it’s worth, I was in NY a couple weeks back and those asking for money are still happy to get a dollar bill.

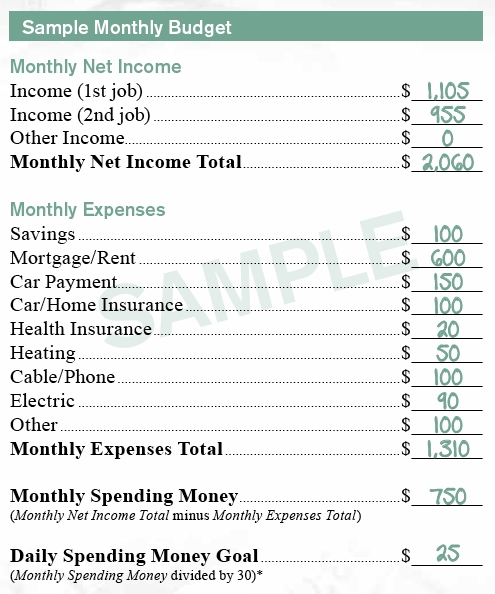

In February I asked is it Time to Raise The Minimum Wage? Recently, McDonald’s (yes, the purveyors of fine hamburgers) offered up a budgeting guide for its employees.

It starts by assuming a second income. Which, in a sense, proves that minimum wage isn’t quite a living wage. I’m struggling with this budget, and trying to understand McD’s motive for it. If it’s an attempt to make the case that this income is enough to survive, it clearly misses the goal. Last I checked, if you don’t eat, you die, eventually. Where do you see food on this budget? Clothing? Haircuts? (I did go nearly a year without a professional haircut, but my wife and daughter put a stop to the home cuts.)

I’d also like to know where one can get a health insurance policy for $20 per month.

As I mentioned in my minimum wage article, I remember $3.10 an hour. For me, it wasn’t a living wage, it was beer money. My attitude back then was “I spent most of my money on women and beer, the rest, I wasted.” But even then, I had coworkers who weren’t high school or college students, they were adults for whom this money was their family income. I don’t know what their spouses did, hopefully this was a second income. As I see the unemployment rate refuse to drop as it should in any real economic expansion and I hear that people aren’t returning to full employment, but a hodgepodge of part time work, I’m concerned about where the middle class is heading.

Can you live on the budget above? What else do you see missing?

I’ve been away for a bit, but still reading my fellow finance bloggers, so here’s my latest roundup of the ones that really impressed me –

Let’s start with The best mortgage term: 10 years at Preretired.org. Preretired Nick makes a great case for what now appears to be an ultrashort term loan. You see, the 30 year loan wasn’t the mortgage of choice, not until after the Great Depression. But, let Nick share the details with you, it’s an insightful article.

At Mighty Bargain Hunter, John shared Soup to nuts: Preparing meals to save money, a discussion on how to reign in the cost of cooking. Given how food is such a large chunk of the typical budget, this is a great place to start.

Two class action suits came to my attention, one for Naked Juice, the other for Barbara’s Bakery. You don’t need any proof of purchase just yet, after all, who saves detailed store receipts, but you might in the future. We’ve used products from both companies, let’s see if they give us back a few dollars.

Barry Ritholtz shared his Favorite “Non-Boring†Business Books. I now have a number of new books to add to my reading list. Sometimes reading these books will help you avoid disastrous mistakes others have made. Better to learn from history than to repeat it.

Next, a Major life event update from Stephanie. She is a fellow Massachusetts-based blogger, and broke the news this week – She’s engaged. I wish her well. Jane and I will soon celebrate our 19th anniversary, so despite all the divorce statistics, a marriage can last a long time. Good wishes to you, Stephanie, I’m looking forward to hearing about your big day.

We’ll wrap up the week with Len Penzo’s Why Pastry Chefs Are Financially Savvier Than The Common Man. I won’t even try to explain the connection, you’ll just have to read it for your self.