This is the week many kids go back to school. To some, it feels like a life sentence, it I think these years go by way too fast. Enjoy the time when you are still young.

This is the week many kids go back to school. To some, it feels like a life sentence, it I think these years go by way too fast. Enjoy the time when you are still young.

Today, a guest post from Ryan.

A few months ago we talked about the benefits of DIY investing vs. hiring a financial planner. There are definitely reasons to go both routes. Maybe you thought that the DIY approach was your best option but after six months of trying to go it alone (albeit with the help of sites like 1Wealth Trading to help you master the basics) you’ve decided you’d feel safer hiring a financial planner to help you get your portfolio (and financial future!) on track.

So how do you do that?

1. Beware the Commission

Before you even meet with a financial advisor or planner, find out whether or not that person is working on salary or commission. It is always better to work with someone on salary. Why? Because commission based financial planners and advisors only make money on what they sell you for your portfolio. This makes it harder for them to resist taking risks with your investments. You don’t want to have to worry about your planner’s motivation.

Note: Obviously not every commissioned financial planner is going to sell bad stuff to make a commission! Most commissioned advisers and planners are highly honorable people. But do you really want to have to wonder about the person’s motivation?

2. Look for the CFP Certification

Believe it or not, most financial planners only have to pass two tests to be considered “qualified†to sell investments and insurance. From there, they can go on to purchase a lot of other certifications to help them add credibility to their reputations. Sorting through all of the certification initials after a planner’s name can be difficult and confusing. The certification you want to see the most is CFP®. In order to obtain this certification, the planner is required to go through extensive training, testing, pass a background test and have three years of full time experience to their names.

3. Experience Matters

CFP certification requires a minimum of three years experience, but it’s good to go with a planner who has been on the job for a while. The lengthier your potential planner’s history, the more experience he or she has with finance as an industry. The “greener†your planner or advisor, the more likely it is that he or she is relying on sales training than any sort of practically built financial experience. A good rule of thumb is ten years. Ten years is the average length of a market cycle.

4. References Matter

Always always always check a potential planner or advisor’s references. Get these references from multiple sources as well. You don’t want to rely solely on the references given to you by the planner you’re interviewing. Ask around to see who your friends and colleagues choose to work with. Run your potential advisor or planner’s name up the proverbial flagpole to see if your friends or colleagues have heard of him or her before and to find out what sort of impression they got. Do an actual background and reputation check on every potential candidate. This includes double checking certifications, checking with the BBB, etc. It’s better to be safe than sorry. After all, it’s your money, right?

Finding and choosing the right financial planner or advisor isn’t something you can do with a quick Google search. This isn’t online dating (though it can feel that way sometimes). You need to actually spend time with and thoroughly vet every potential candidate before you trust anybody with your money and your financial future.

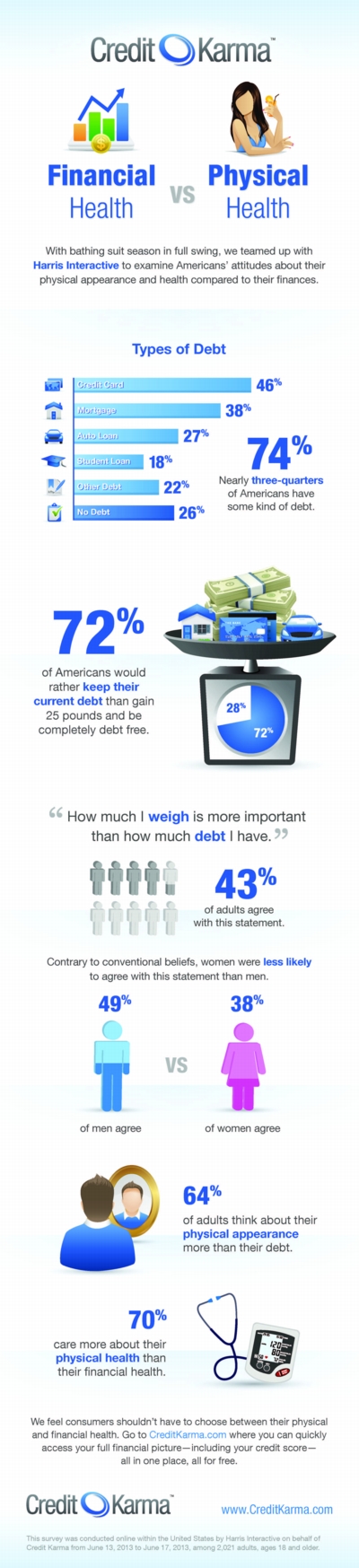

My friends at Credit Karma enlisted the help of Harris Interactive (the famous “Harris Poll” people) to take a look at how people prioritize their financial health and their physical health. The results were a surprise to me. With money at the top of the list of things keeping people up at night, I’d have thought being debt free would rank pretty high. Check out this infographic, and click on it to be taken to the full article at Credit Karma.

Why not leave a comment? Tell me, what’s more important to you right now, your weight, or your debt? No cheating, you can’t say, “both!”

Let’s start this week’s roundup with Ron’s post at The Wisdom Journal, Retirement Advice That Goes Against The Grain. Ron offers four tips, each of which, taken as a soundbite, sounds a little crazy. However, when you read Ron’s discussion of each bit of advice it paints a pretty sane picture of how to approach retirement planning. A nice read to start the week.

20 Something Finance’s GE Miller suggested you Calculate the “Total Cost of Homeownership†BEFORE Renting or Buying. As I read it, I thought how what became obvious over time to us older folk may not be on the mind of the young home buyer. Don’t get into a new purchase or rental without understanding the total cost. GE continues to put out some quality writing.

How many of you invest outside of retirement? Ninja asks this at his site Punch Debt in the Face. Once you’ve saved up that emergency fund and are handling your budget just fine, are you saving only in the retirement account, or other accounts as well?

Rick Ferri (whom I met last year, nice guy and interesting to talk to in person) explained why Splitting Growth And Value Leads To A Worse Return. Rick discussed how some advisors use an equal share of each, which struck me as silly as well. On the other hand, if one is prescient enough to choose the one that will outperform each year, there might be some extra money to be made. If your advisor has you in the Russell 1000 Growth and the Russell 1000 Value, show them Rick’s article and ask them to explain why you’re paying a higher expense than the plain Russell 1000.

The Reformed Broker, Joshua Brown, made The Case for Brazil, the World’s Most Hated Stock Market. His article started “Gun to my head – I had to pick a single non-US stock market to be invested in for the next ten years and I cannot touch the money in between, which one would I pick? I don’t even need to think twice about it, the answer is Brazil.” Pause. The next day, Josh posted What Happens When You Buy Brazil Down 20%? In this follow on discussion he offered some history, how the Brazilian market fared 6 months after falling 20%, and the numbers are impressive. Up 90% of the time with an average 30%+ gain. EWZ is the ETF I chose to use to invest in the Brazilian market. Josh’s site warns Nothing on this site should ever be considered to be advice, research or an invitation to buy or sell any securities, and I’d like to echo that. Personally, I think that we in the US can easily load up on US stocks, S&P ETFs, and miss the diversification the rest of the world can offer.

The Mighty Bargain Hunter asked 10-year mortgages: How low can you go? A great discussion, and the only red herring in the article is the ratio of interest to principal in the payment. You know, early on with a 30 year mortgage, the principal is a tiny part of the payment and it increases each and every month. John offers that there’s a good feeling when you start out with most of you payment going to principal. That may be, but not for me. My mortgage duration is tied to my target retirement date, if I were in my 20s or 30s, I’d be sitting on a brand new 30 year mortgage, and when inflation returns, I’d watch it devalue itself faster than I’m paying it off.

I’ll admit, I hadn’t eaten a Twinkie in 20 years, but when I heard Hostess was bankrupt, I began to miss them. Now that Twinkies are back, I bought a box, and offered my 14 year old daughter her first Twinkie. She took one bite and wasn’t impressed.