by Joe

on February 2, 2013

4th quarter GDP shrunk by .1%. Are we heading toward another recession? Have we expanded our way out of the last one? A double dip recession can occur when the economy starts to shrink after only a quarter or two of growth. With two years of growth, even slow growth, behind us, a recession would be a new recession, not a double dip.

That said, defense outlays dropped by a 22% rate in Q4, and given how large this spending usually is, it accounted for all of the dip we just saw. Jobs showed an increase of 192,000 according to my friends at ADP, the payroll processor. And the market (measured by the S&P 500) shrugged off the news gaining nearly a percent for the week.

{ }

by Joe

on February 1, 2013

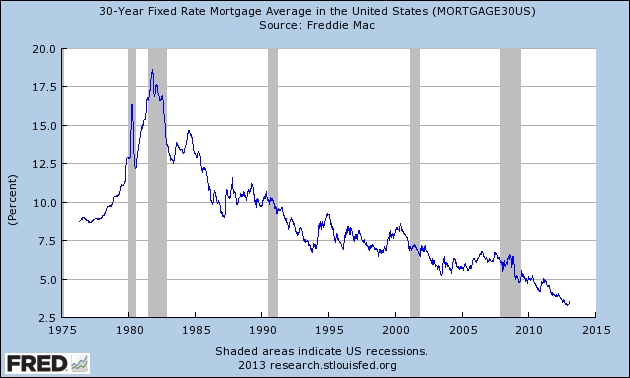

I’ve been hearing more confusion lately regarding how and when it makes sense to refinance your mortgage, and thought we’d discuss it a bit today. First, the obligatory graph –

You can see that as recently as 2009, rates were still above 5% and in the 7’s earlier in the decade. This is well above today’s 30 year rate of 3.4% or 15 year rate of 2.7%. Still, there are people who are under the misconception that a refinance on a 30 year mortgage makes no sense if you are half way through it. Nonsense. (Because on a family friendly site, I’m not supposed to say Bull****) It might be silly to refinance when there’s only a year left to go, but you should do the math and see what makes sense for you.

The way a mortgage is paid off, with a 5% rate, a 30 year mortgage will have about half its balance after 20 years. So, with $100,000 left on that $200,000 mortgage, you find a 15 year rate of 3%, higher than I mention above, but with no closing costs. You see that you were paying $1073 per month, and the new payment will be $690. What to do? Here’s the key point – go back and calculate the payment should you choose to use the new rate but pay it off in the 10 years that remain. You see $965. By refinancing and making payments to stay with the remaining term, you still save nearly $110 per month. Each and every month for 10 years. Not bad for a few hours effort to gather up the paperwork.

Should you take the new payment offered? If you have a car loan or other high interest debt, the extra $380 might help you save quite a bit in interest. Are you depositing enough to your 401(k) to get the full match your company offers? You might deposit that $385, pre-tax and have it doubled on deposit. When 10 years pass, the extra money in the 401(k) will far exceed the remaining mortgage balance. The important factor to consider when comparing loans is how the payments compare when using the same term that remains on the old mortgage. It’s easy to drop your payment by extending the loan to 30 years every time you refinance, but that’s a losing game, at some point you want to put the loan behind you. Tonight I answered a question Are there downsides in refinancing with 5 and 1/2 yrs left? I agreed with the fellow asking the question, it’s a good deal, he’ll save nearly $4000 over the remaining 5 years of his mortgage by refinancing.

{ }

by Joe

on January 28, 2013

For nearly all my adult life, I’ve been using one sort of Reward Credit Card or another. It’s one thing to get miles you may have a tough time using, and quite another to watch as a 529 college savings account funded with these rewards is on track to pay for a full semester of my daughter’s college. I’ve ignored the series of articles that reference “studies that prove consumers spend 12.3% more on credit cards than with cash.” It’s not that I think such things are possible. Nor do I think myself immune to the attraction of the impulse buy. It’s simply that there is no study I’ve found which offers real world data. Giving college students $20 and a $20 gift card to compare behavior isn’t the kind of study that will convince me of anything.

That said, I don’t kid myself into believing there’s no cost to this. The money in that 529 account came from somewhere. I’ve always known that the credit card companies are making money both on the interest paid by those who carry a balance month to month, and from the fee they charge the merchants to process the transaction. One can rationalize that I’m getting back the money the bank charged the merchant or that the merchant’s profits are lowered by picking up the tab. Worse, others have suggested that the merchants are all forced to charge more and prices are all a bit inflated due to the bank’s fees.

The banks also required the merchants accepting their credit cards to not charge extra for credit transactions. In a victory of the Merchants vs The Banks, this was deemed illegal, and starting yesterday, merchants are allowed to add a ‘swipe fee’ for card usage. Interesting to note that ten states have laws restricting any type of surcharge fees: California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma, and Texas.

My advice if you don’t live in one of these states is to pay close attention. Stores that plan to charge an adder for a credit card transaction need to post it clearly near the register. If the fee is more than your reward, you might wish to consider going back to cash. (Except for the fragile tech tech purchase on a card that offers a year’s damage protection. That’s worth every bit of a percent or two to me.)

{ }

by Joe

on January 27, 2013

Let’s start this week with The Embarrassment of Having a Check Denied at the County Clerk’s Office. Kevin at No Debt Plan shared some details that may have been embarrassing, but also should serve as a great lesson to the rest of us. Read the whole article and think twice before you turn up in person with a check.

At Lazy Man and Money, a guest author gave us Easy Things You Can Do to Save You Money. Just shy of a ‘Top Ten’ list, Sara Masterson offered some nice ways to find some extra money at the end of each month.

Len Penzo explains Why a Million Apples a Day Couldn’t Keep the Sellers Away. As part of Len’s view of the world he posts weekly, Len discusses politics, the economy, and more. This week he offered some numbers regarding Apple, such as they sell 1 million products per day. Looks like they are oversold right now, and I’ll bet they’ll be back to record territory by the end of this year.

I’m pretty good keeping up with financial news. New tax code? I often know the details within a few hours of the details breaking. Which is why it’s great to find a gem of information I was unaware of. At 20 Something Finance, GE Miller explained the New Federal “Pay As You Earn†Student Loan Repayment Plan Now Available. It’s just like it sounds, a plan that lets workers pay off their loan at a rate based on a percent of their income. Glad to see this option has become available.

We’ll close this week with 4 Things You Should Know about Filing Your Taxes in 2013. I’ll admit it – I only went 3 for 4, so I’m glad I read Miranda’s article.

Now, about that Luxating Pattela. My little friend’s knee has been dislocating and causing him some discomfort. Yes, that’s a tail you see in his X-ray, it’s my 1 year old puppy. The first time this happened was a few weeks back, scared the heck out of me, he screamed and held his leg off the ground. Fortunately, I figured out what was going on and was able to pop it back in, but the issue is recurring and the Orthopedic vet advised surgery was indicated. It’s not going to be cheap, but fortunately, we have insurance that should cover this with a 10% copay. His surgery is tomorrow.

{ }

by Joe

on January 25, 2013

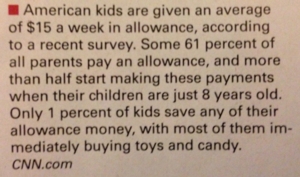

I was going to title this post something like, “My Daughter, The One Percenter.” I know each of us thinks our own child is special, but it never hurts to get some extra validation. Independent data that proves it beyond a doubt. A brief story from CNN talking about kid’s allowance and savings was interesting to me –

First, Jane2.0’s allowance happens to be the $15 average. We started giving her the number of dollars to match her age, at about 7 or 8. Now, at 14, I round up, so $15 it is. It’s the 1% that surprised me a bit. In the age of gadgets and electronics, a week’s allowance isn’t enough to buy much, and I’d have imagined more kids would be savers. When J2 wanted a MacBook laptop for her birthday, we said that $1000 was more than we were planning to spend on a 12 year old’s birthday present. We agreed to pay for half, and she would take the other half from her savings. We felt this served as a good lesson, the benefit of saving her allowance and money she started to earn babysitting, and it would also prompt her to be more responsible with the laptop.

Enough bragging, she’s off to a good start, understanding the value of money and learning that the cost of a purchase can be converted to the number of hours of babysitting or week’s worth of allowance to buy the item. How about the 99%? All of the kids who are getting an allowance but spend it as fast as it comes in? It seems this snippet of a story may be the preface to the longer tale of the low saving rate in the US, and why at the back end so many have failed to prepare for retirement.

{ }